Mobile market overview

Peru had a population of 31.0 million people and 31.4 million mobile subscriptions at the end of 2014, giving a mobile penetration of 101% - the lowest level of penetration of the major countries of South America. Around 68% of subscribers had a pre-paid account.

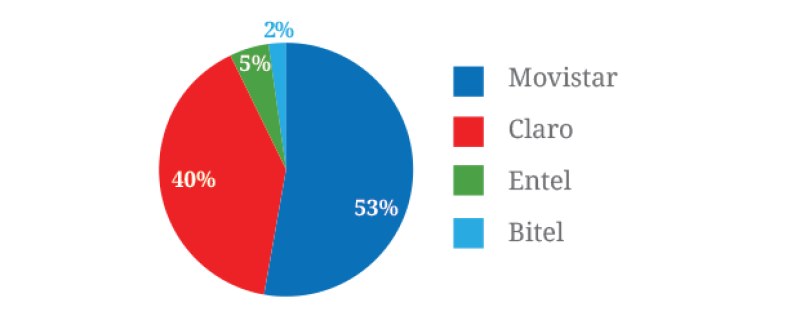

There are four Mobile Network Operators (MNOs) serving the Peru market (See figure 1), with two companies dominating the market – Movistar (Telefónica) with 16.8m subscribers and Claro (América Móvil) with 12.5m.

Mobile subscriptions- market share

Key Mobile Developments

Whilst Peru has a relatively low level of mobile penetration for the region – certainly when compared to markets such as Argentina and Uruguay which have over 150% penetration – it is showing a healthy level of growth. There were over 1.2 million new mobile subscriptions in Q4 2014 alone.

In terms of mobile technologies, Claro launched 3G services back in 2008, followed by Movistar and Entel the following year – and by the end of 2014 there were 10.7m 3G subscribers (34% of subscribers).

The advent of 4G

2013 saw the auction and sale of two twenty years 40MHz (2×20MHz) spectrum licences in the 1700MHz and 2100MHz paired bands (also known as Advanced Wireless Services [AWS] spectrum) for 4G services – following a process run by the Agency for Promotion of Private Investment (ProInversion). Movistar secured the ‘A’ block of 1700MHz/2100MHz frequencies for US$152.2m – more than twice the reserve price. Americatel Peru (owned by Chile’s Entel), won the ‘B’ block of AWS spectrum for US$105.5m. There had been four bidders for the spectrum – the other two companies being Claro and Viettel.

The fact that Claro did not secure spectrum is significant – although it has subsequently found a work-around by employing a 1900 MHz band previously used to deliver 2G services, which had become largely redundant. Claro has thus far been able to justify this move by arguing that regulation does not specifically forbid the delivery of 4G via other frequency bands – and indeed 4G networks have been successfully implemented via 1900 MHz bands in other markets. Claro has thus been able to launch 4G services despite losing out in the initial auction.

As a result of these developments GSMA estimates that there were just over 1 million 4G subscribers at the end of 2014.

A second 4G spectrum auction is currently being run by ProInversion – this time for three blocks of spectrum in the 698MHz-806MHz band – a process which is scheduled for completion in Q2 2015. The three lots on offer are as follows: Block A, 703MHz-718MHz, 758MHz-773MHz; Block B, 718MHz-733MHz, 773MHz-788MHz; and Block C, 733MHz-748MHz, 788MHz-803MHz.

Operator Activity

Market leader Movistar has announced a series of investments in mobile infrastructure over the last few years – including plans to spend US$400m on LTE over the five years following its launch. Following its acquisition of 4G spectrum, Movistar announced the intention to roll-out LTE services across 234 towns and district capitals – and indeed it was obliged to launch services within a year, covering 114 district capitals, under the terms of its concession.

Movistar duly launched LTE services in seven districts of Lima in January 2014, expanding coverage to twelve new areas of the city by the middle of the year. This was followed by expansion to Trujillo and Arequipa. By late 2014 its 4G network was reported by La Republica to cover 52 districts across Peru – 36 of them in Lima. GSMA estimates that by the end of 2014 Movistar has secured just under 500,000 4G subscribers.

At the same time in 2014 the company announced plans to expand its mobile service coverage to 2,327 rural locations – part of a rural roll-out programme mandated as a condition of its license renewal in 2013. According to Telecompaper, by December 2014 it had extended its services to 1,432 new locations. At the end of 2014 Movistar also announced plans to roll out fixed wireless internet access in the Amazon region of Peru, in conjunction with Ericsson.

According to newspaper Gestion, Claro is also planning to invest significantly in the Peruvian market – with close to US$1bn earmarked over the next three years to expand coverage and boost capacity. It plans to invest over US$300m in its 4G network. Claro has also claimed that its 4G customer reached 600,000 users by the end of 2014 - although GSMA puts the figure at just over 500,000 – having launched services in May 2014.

Entel likewise announced plans to invest heavily in its Peruvian operation, with c. US$1.2bn pledged for the period 2015-2020 and the ambitious objective of boosting its market share from 5% to 30%. Following its successful acquisition of 4G spectrum in 2013, the company announced that its subsidiary Americatel Peru would spend over US$400m rolling out 4G coverage to around 200 districts.

Entel launched 4G services in the Q4 2014 although GSM estimates that it had only a few thousand subscribers by the end of the year.

2014 also finally saw the launch of Bitel – which according to the Telecoms Regulator Osiptel had struggled to secure permissions from municipal authorities for the installation of towers. Its owner, Viettel, was awarded 25MHz of 1900MHz spectrum in January 2011 and went on to win frequencies in the 900MHz range. Viettel pledged to provide free broadband services to more than 4,500 educational and healthcare institutions for ten years, and is obliged to provide mobile services to 48 underserved rural districts within the first 5 years.

Whilst Bitel had stated a target of securing 500,000 subscribers by the end of the 2014, GSMA estimates that it had just over 100,000 subscribers by that time.

In addition to the four Mobile Network Operators, a number of other communications providers have announced plans to roll out infrastructure and services.

In late 2014, WiMAX provider Olo stated plans to invest US$88m over the next five years rolling out 1,000 LTE BTS, starting in mid-2015 – subject to gaining the required permissions from the Ministry of Transport and Communication (MTC). Olo envisages providing its full suite of services through the network, to more than 80 cities in the provinces, in an effort to increase the brand’s adoption outside of Lima, which currently accounts for 99% of its sales. At the time its WiMAX service was available in 24 districts of Lima and 12 other cities.

According to Comercio, DirecTV also announced plans in late 2014 to launch LTE services in Q1 2015 using 2300MHz frequencies previously allocated to Digital Way. DirecTV was reportedly planning to use this platform to offer fixed-wireless residential services, but the operator has apparently not ruled out entering the mobile market in the future.

In February 2015, Venezuelan-backed ISP Movilmax launched in Peru, with a 2.5GHz WiMAX network covering San Isidro, Miraflores and Surco (in the Lima province).

The tower sharing market

The authorities in Peru have been making positive noises about facilitating the roll out of more tower infrastructure – something imperative if all the investment plans above are to come to fruition. In mid-2014 MTC urged local authorities to cooperate with providers regarding the deployment of telecoms infrastructure, noting that a number of operators had encountered difficulties in obtaining municipal permits to install aerials.

In early 2015, Regulator Osiptel proposed changes to the Telecommunications Act that would enable mobile operators to apply for permission to install antennas on public buildings. According to TeleSemana, the amendment is intended to assist operators struggling to increase coverage and service quality due to the aforementioned difficulties in acquiring the necessary permissions from municipal authorities. Claro Peru’s regulatory affairs director Juan Rivadeneira was quoted as saying that as a result of these issues, Peru has one of the lowest antenna per capita ratios in the world.

Nevertheless, Peru already has a number of active tower companies, including key international players – such as American Tower (AMT), which entered the market back in 2010, and Torres Unidas – as well as Torres Andinas, NMS, Torresec Peru and a number of other local towercos. SBA has been reported to be looking for opportunities in this part of South America. The market appears to be a fertile one for towercos – and indeed Torresec Peru has been quoted in the past in TowerXchange saying that it has experienced relatively few difficulties securing permits in Peru – with is sometimes taking as little as one month to obtain a response once a request for permits is presented.

There are estimated to be around 9,000 towers in Peru in total, with around a fifth in towerco hands. AMT has the largest number – 571 – and Torres Unidas around 350 towers. There is believed to be a need for at least another 14,000 towers.

Conclusions

The Peruvian market has many positive characteristics with regard to its potential for towercos. With 30 million inhabitants and only 101% mobile penetration, there is significant potential for subscriber growth. 4G services have been launched, new 4G spectrum is on the point of being released, and all the MNOs have announced significant investment in network expansion – both for 4G, 3G and to meet coverage targets for rural areas. At the same time the market is underserved with tower infrastructure, has an active towerco market, and has regulatory authorities well disposed towards reducing red tape. Mott MacDonald believes the market is therefore likely to see both the entry of new players as well as consolidation amongst existing parties, as the full potential of the market is realised over the next few years.