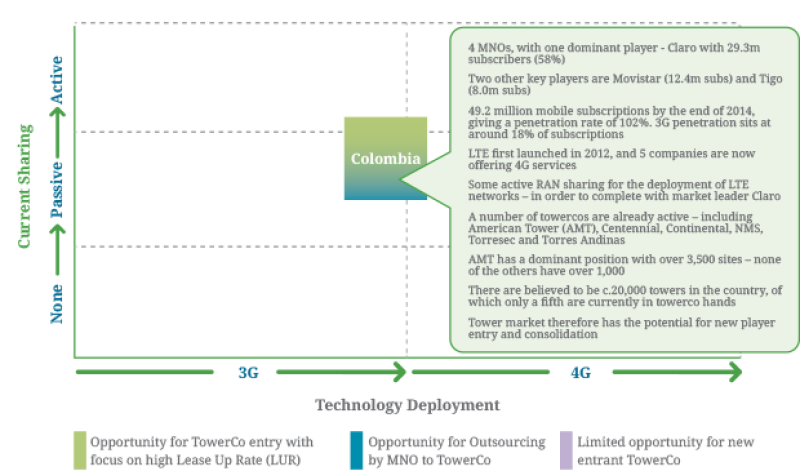

Colombia had a population of 49.2 million people and 50.2 million mobile subscriptions at the end of 2014, giving a mobile penetration of 102% - the third lowest level of penetration of the major countries of South America (slightly ahead of Peru’s 101%). Around 80% of subscribers had a pre-paid account.

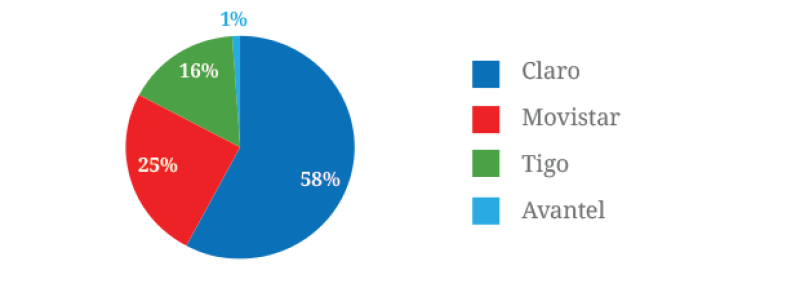

There are four Mobile Network Operators (MNOs) serving the Colombia market (See figure 1), with one dominant company – Claro (América Móvil) with 29.3m subscribers – and two other significant players – Movistar (Telefonica) with 12.4m subscribers and Tigo (Millicom) with 8.0m. Fourth player Avantel has fewer than 500,000 subscribers at the end of 2014.

Mobile subscriptions- market share

Key Mobile Developments

Colombia has a relatively low level of mobile penetration for the region, but showing healthy growth – with close to 1.5mn new mobile subscribers added in Q4 2014. 3G services were launched back in early 2008, with Movistar initially leading the way – although by the end of 2014 there were still only 8.9mn 3G subscribers - 18% of all mobile subscribers, a relatively low proportion.

The advent of 4G

As far back as June 2010, Une-EPM Telecomunicaciones won a tender for mobile spectrum in the 2500MHz-2690MHz frequency band, which the company used to deploy LTE. Une paid US$4.05mn for each of ten spectrum blocks of 5MHz. Une then launched the nation’s first 4G network in June 2012. Five companies subsequently won 4G spectrum at an auction held in mid-2013: Movistar (which paid US$103mn for 30MHz in the AWS [2100MHz/1700MHz] band), a consortium formed by ETB and Tigo (US$102mn for 30MHz in the AWS band), Avantel (US$56mn for 30MHz in the AWS band), DirecTV (US$37mn for 30MHz and separately US$37mn for 40MHz in the 2.5GHz band), and Claro (US$62mn for 30MHz in the 2.5GHz band). The bid from Mexico’s Azteca 4G was unsuccessful and the auction for spectrum in the 1900MHz band was declared void.

Rollout targets for winning licensees were set at 50% of all municipalities by July 2014, increasing to all areas by 2018, though the network obligations were relaxed for new entrants. Claro will be restricted to bidding in the 2500MHz band, whilst Tigo and Movistar will be limited to the 2100MHz and 1900MHz ranges.

By the end of 2014 GSMA estimates that there were 1.7mn 4G subscribers in Colombia, with Claro leading the way with just over 700,000 subscribers followed by Tigo with 500,000 subscribers (having merged with Une in 2014) and Movistar with 340,000. Avantel and ETB were also providing 4G services.

In late 2014 the Ministry of Information Technology and Communication (MinTIC) and the National Spectrum Agency (ANE) prepared a draft resolution regarding the proposed distribution of spectrum in the 900MHz and 1900MHz bands. The planned tender will comprise 22MHz of spectrum in the 900MHz band (894MHz-905MHz paired with 939MHz-950MHz) and a 5MHz block in the 1900MHz (1850MHz-1990MHz) band. Mobile operators which manage to secure spectrum will be obliged to offer preferred national roaming rates and share infrastructure, among other conditions. In addition, 1900MHz spectrum winners must extend services to 40 inaccessible locations, while 900MHz licensees must offer connectivity in 50 unserved areas.

Operator Activity

Claro has launched 4G services in Bogotá, becoming the fourth operator to offer LTE in Colombia. As of August 2014 it claimed to have rolled out 4G services to 95 municipalities and 28 municipal capitals – having invested US$1bn over the last three years – the first phase of plans to extend 4G coverage to more than 600 municipalities over a five year period.

Movistar launched commercial LTE services in Bogota, Medellin, Barranquilla, Cali and Bucaramanga in early December 2013. A year later it announced that its post-paid 4G user base has reached 300,000, with service available in 75 major cities and municipalities – surpassing its regulator-stipulated coverage commitments. The coverage requirements set by MinTIC stipulated that it should offer services in 58 department and municipal capitals within a year of launch – with roll out of LTE to 313 municipalities obligatory by 2018.

Une-EPM was the first operator to launch an LTE network in Colombia, and the company successfully merged with Tigo Colombia in August 2014. The merger allows the combined entity to offer a full range of fixed and mobile voice, data and TV services. As part of the deal, the recently merged companies have agreed to relinquish a 50MHz block of spectrum in the 2500MHz band. The decision was ordered by the Superintendencia de Industria y Comercio (SIC), after the spectrum holdings owned by the combined entity grew to 135MHz, well above the stipulated 85MHz limit. By February 2015 the merged entity had achieved LTE coverage of 75 cities.

Digital trunking provider Avantel was awarded 30MHz of airwaves in the advanced wireless spectrum (AWS) band (1700MHz/2100MHz), and engaged Nokia Solutions and Networks (NSN) to roll out its LTE infrastructure. It launched services in Q3 2014 offering the platform in 20 cities, whilst a national roaming agreement with the incumbent MNOs has granted the operator 3G coverage of 1,100 municipalities – after the Communications Regulation Commission (CRC) backed the new entrant in its bid to oblige the incumbents – Claro, Movistar and Tigo – to open their networks to Avantel for automatic national roaming. This was given that they were obliged, under the terms of their 4G licences, to provide national roaming for newcomers to ensure their smooth entry into the wireless market. By late 2014 Avantel had reportedly extended its 4G footprint to 27 cities. Going forward, the operator stated plans to cover 57 locations by mid-2015.

In 2014 state backed broadband provider Empresa de Telecomunicaciones de Bogota (ETB) announced major investment plans for the next year, including the launch of its own mobile network, according to newspaper Portafolio. Having purchased 30MHz of AWS (1700MHz/2100MHz) spectrum in partnership with Tigo Colombia, ETB planned to scrap its mobile virtual network operator (MVNO) arm in favour of operating its own network.

Finally, DirecTV also launched its 4G service in July 2014, branding the new offering DirecTV Net. DirecTV aims to cover 57 municipalities in the next five years, and had already extended its footprint to 18 cities by late 2014.

Regulation

Colombia’s Communication Regulation Commission (CRC) has attempted to address some key issues hampering the development of the mobile market in recent years, with mixed results.

In 2013, for example, CRC finalised measures to be taken against dominant cellco Claro designed to diminish its degree of market dominance. Legislation looked to impose a market share cap, limiting players to controlling no more than 30% of the nation’s mobile subscriber base. If passed, the bill would have required Claro to halve its market share. However, a senate committee voted 6-3 to drop the bill, arguing that the constitution already features ample measures to address anti-competitive behaviour.

In 2013 a Constitutional Court in also stated that Claro and Movistar must hand over their entire telecoms infrastructure in the country once their concessions expired in March 2014. The two firms had thought that the expiry of the licences meant that only their spectrum would have to be returned, but the Court upheld an earlier decision by the State Comptroller which ruled that all network equipment would have to be included. Six companies were licensed to begin operating in Colombia in 1994 using equipment inherited from the former public monopoly. Under the 1994 licences they agreed to return their assets to the state once the concession period had ended – an agreement still deemed to be pertinent to Claro and Movistar and one potentially meaning they would have to acquire new spectrum licences and sign wholesale infrastructure deals if they wished to continue offering services.

In the event, in March 2014 the Colombian government agreed to renew the operating licences of Movistar and Claro for a further ten years, adding further quality of service requirements to the new concessions. Under the deal, the duo were required to renew their rights to 15MHz each in the 1900MHz band and 25MHz in the 850MHz range. The new concessions carried increased demands for service quality which, if not met, will potentially lead to the MNOs having their sales to new customers restricted.

In late 2013 a Colombian senator also proposed the establishment of a state-sponsored tower company to manage the nation’s wireless tower infrastructure and lease capacity to operators. It was argued that nationalising the country’s tower assets would improve coverage and competition, as all operators would have access to all towers. However, this proposal did not come to fruition.

The tower sharing market

There is already a highly active towerco market in Colombia. American Tower (AMT) is the market leader, with a reported 3,589 sites, and companies such Centennial, Continental, NMS, Torresec and Torres Andinas are also present – and early portfolios are being developed by Phoenix Tower International and Torres Unidas, among others. As reported previously by TowerXchange, while Colombia has numerous towercos, only AMT has a quadruple digit tower count in a market where towercos own a little over 4,000 of the c.20,000 towers in the country (c. 20% of towers).

It has also been reported that Movistar and Tigo have engaged in active RAN sharing for the deployment of their LTE networks – in order to better complete with market leader Claro. And whilst a National Law diminishes some of the issues around new site permitting, municipalities have a degree of freedom to block or shut down a site if considered in the public interest. This can lead to delays as negotiations take place with local authorities and communities.

However, with the amount of LTE activity and demand for sites from a range of players – as well as a thriving MVNO market driving further subscriber growth – such issues are viewed as an inconvenience to towercos rather than a significant brake on their development

Conclusions

With a large population of around 50 million people and mobile penetration only just above 100%, there is considerable room for subscriber growth in the Colombian mobile market. 4G services have been launched and take-up is growing fast – and the level of 3G penetration is relatively low – meaning that there is likely to be a demand for the infrastructure to support both 3G and 4G roll-out in the medium term.

The degree of market dominance of Claro is not ideal from a towerco perspective – given that its future strategy with regard to infrastructure sharing and ownership of its towers will have a disproportionate impact on the market. However, as the presence of a number of leading and local towercos testifies, any risk present is outweighed by the future potential of a market in which a significant increase in the tower stock will be required to realise the ambitions of myriad mobile market players.