While in Brazil, many executives I met were still wondering why AT&T hadn’t invested in South American telecoms. The rumour has been going on for so long, people started to refer to it as a urban myth. Of course in the meantime, AT&T put US$67bn on the table to acquire DirecTV, a transaction which is now under review by the Federal Communications Commission (FCC). Although not technically related to telecoms, the move was just the initial step of AT&T shopping spree in the CALA region that has since been followed by acquisitions in Mexico. I am intrigued about the implications for the tower industry in both the U.S. and Latin America.

AT&T acquisition strategy South of the border: from pay-TV to Mexican MNOs

DirecTV is the second largest pay-TV service in the United States behind Comcast, and has a total of over 18 million subscribers in Latin America (split between DirecTV Latin America and Sky Brasil). The pay-TV industry is expanding in CALA thanks to the growth of a young middle class and to date, it has a reported 40% penetration rate.

Just a few weeks later, AT&T made the headlines in the region but not for any Brazilian acquisition. Over the course of a few days, the U.S. giant signed agreements with both Grupo Salinas and NII Holdings for the acquisition of their Mexican operations, namely Iusacell and Nextel Mexico. While the Iusacell merger is now complete, the Nextel acquisition remains subject to regulatory review. In the meantime, through its Iusacell deal, AT&T gained control over 9.2 million subscribers in Mexico, which could become 12.4 million should the Nextel deal get approved.

Although not even close to the 71.3 million users of Telcel, AT&T could become a serious competitor both to América Móvil’s market leader and to Movistar, Telefonica’s Mexican carrier, which serves more than 18.3 million customers in the country. In the meantime, AT&T will add a few more million wireless subscribers to its score - which reached 120 million back in 2014, making it the second largest operator in the U.S. behind Verizon.

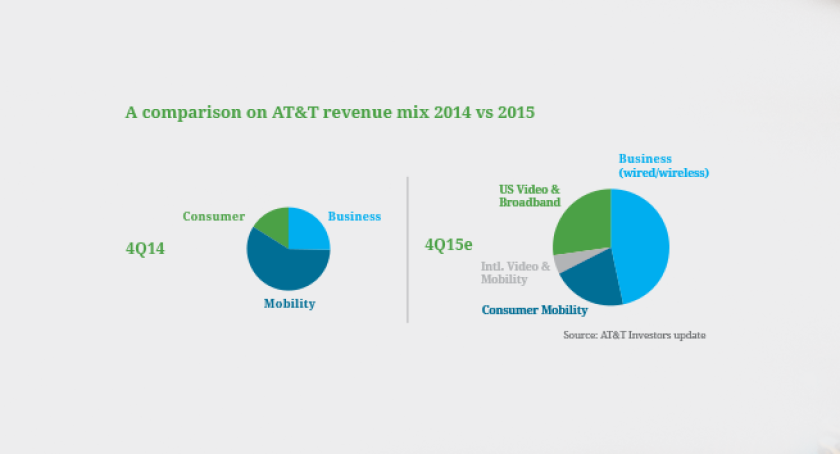

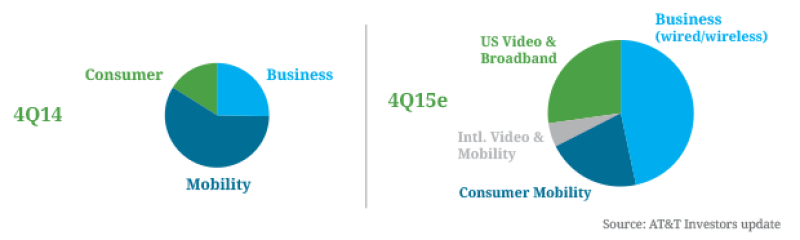

A comparison of AT&T revenue mix 2014 vs 2015

In the meantime, Verizon focuses on its domestic wireless business

Looking at Verizon’s growth strategy, one thing is obvious. It couldn’t be more different than AT&T’s. A few weeks ago, Verizon’s CEO Fran Shammo denied that the company is interested in América Móvil’s towers and stressed in an interview with the Wall Street Journal that there’s no plan to invest in Mexico nor Latin America.

A few weeks ago, American Tower agreed to pay US$5.05bn to acquire rights to 11,324 telecom towers and buy an additional 165 sites from Verizon. This latest substantial tower divestiture is in line with Verizon’s strategy to focus its attention entirely on its wireless business.

Back in February 2014, Verizon paid an astounding US$130bn to acquire full control of Verizon Wireless by acquiring Vodafone’s 45% interest in the company. The transaction contributed to consolidating the company’s position in the wireless market but also to raising Verizon’s debt from US$50bn to US$113bn over a few months; hence its decision to divest its towers and other nonessential assets. However, thanks to the acquisition, Verizon Wireless reported an 8.2% growth YOY and represented 70% of the company’s overall revenue.

Is diversification the right move?

The implications for AT&T and Verizon’s strategies have to be analysed in light of the ongoing and cut-throat U.S. price war among carriers. As new subscribers are tough to find in a highly penetrated market, companies seek to attract new activations via competitive price plans, credits and special offers, all contributing to declining ARPUs and reduced margins. And although data consumption is still expected to grow exponentially, carriers won’t benefit as much due to falling data prices.

While American Tower reported 7% domestic core organic growth, compared to 13.5% internationally in their 2014 Q4 results, SBA forecast 9% domestic growth and around 13% international, one of the themes of analyst Q&A during recent webcasts and investor conferences was the slowdown in AT&T expenditure which started at the tail end of FY2014 and which is predicted to continue into FY2015. Whilst there has always been an ebb and flow of capital from the leading operators into their towerco partners in the US, the coincidence of AT&T’s reduced expenditure in the US and the feeding frenzy of build-to-suit activity their entry in the Mexican market has heralded is illustrative of why AMT and SBA are investing heavily in CALA.

In fact, during 2014 AT&T added 3,700 sites to its U.S. portfolio with a slowing trend towards a maximum of 2,000 sites estimated in the period 2015/2016, as recently reported by analyst firm RBC Capital Markets, LLC.

The potential of the Mexican tower market is obvious. América Móvil is being forced by the regulator to decrease its market share from 70% to 50%, while mobile penetration rate hasn’t reached 100% yet (92% as of January 2015), illustrating the country’s great growth potential.

AT&T is moving in the right direction – South of the border

Personally, I am inclined to view AT&T moves, especially the Mexican acquisitions, as highly favourable for the company for a few good reasons.

First of all, Mexico is in need of a strong alternative to Telcel, whose sheer dominance had disincentivised Telefonica Movistar from investing the vast capex required to become a strong second alternative - although in fairness, considerable coverage progress has been made recently. AT&T could bring a breath of fresh air along with its U.S. expertise, budget and strong US dollars to become a serious competitor to Telcel and Movistar, hence pushing Movistar to further invest in the country and creating an even more compelling market for foreign investments.

In the meantime, AT&T has announced its plans to build a unified U.S.-Mexico footprint by including unlimited calls to Mexico in some of its Cricket Wireless plans. For now, the plans will prevent people travelling to Mexico from being hit by roaming charges, but commentators expect AT&T to further enhance its offering and make the Mexico-U.S. rates a huge component of its mobility plans. Effectively AT&T is soon to become the only carrier with offerings spanning North America.

Furthermore, we are all expecting América Móvil to disclose its detailed plans to reduce its market share, which apparently include the creation of a separate entity in charge of leasing up its tower portfolio. However, the company has so far relied on its dominant position to retain its customer base and only a recent law has forced operators to decrease its prices. But in a country with one of the lowest customer longevity rates in the world (Mexico is at 35% behind the UK at 32% and Brazil at 20%), a competitive and fair-priced newcomer could represent a serious threat even for Telcel.

In summary, AT&T looks to have made a smart move in diversifying by betting metaphorical ‘chips’ on both wireless and pay-TV, and on both the US and Mexico (and potentially beyond). In contrast, Verizon is ‘going all in’ on the US wireless market, and divesting towers to finance the bet.