By Frances Rose, Head of EMEA, TowerXchange: A deal between Abertis and Wind, the Italian mobile network operator controlled by Russian telecoms giant Vimpelcom, is expected to close by the end of March. The deal, for a 90% stake in Wind’s tower subsidiary Galata, which owns 7377 towers, is worth €693 million or US$774 million.

The bidders

Abertis’ telecoms business focusses on telecoms, media and public administration, with tower sites to date in Spain and Italy. Currently the most acquisitive of the European towercos, their focus on creating a pipeline of tower acquisition opportunities across the continent in the face of limited competition is moving them quickly into the position of Europe’s largest multi-country towerco. Abertis has also recently confirmed plans to spin out the Abertis Telecom part of the business via IPO to allow them to take advantage of "a market where there are currently many opportunities, particularly in the European mobile telephone towers segment"

Abertis reportedly beat Italian investment fund F2i’s joint offer with Providence Equity Partners, who also backed Helios Towers Africa in their most recent round of capital raising, coinciding with the acquisition of part of Bharti Airtel’s tower portfolio in Q4 2014. Combining Providence Equity Partners’ experience and appetite for the tower market with F2i’s expertise in Italian infrastructure, particularly in the areas of utilities and transportation, they appeared to be strong contenders. However there is no information in the public domain about how the assets would have been managed if their bid has been successful, raising the possibility that they would have either recruited a management team or made a trade acquisition to obtain the necessary skills and processes wholesale.

Other early contenders for the deal were believed to include Italian native, Mediaset-controlled EI Towers, and American Tower. It is rumoured that American Tower withdrew from the process after successfully agreeing deals to acquire over 22,600 towers in deals with TIM in Brazil, Airtel in Nigeria and most recently with Verizon in their home US market. American Tower are however believed to retain ambitions to expand their footprint in Europe beyond their existing portfolio of just over 2,000 towers in Germany.

Drivers for the deal

As with all significant tower deals, the sale of a tower portfolio allows operators to release cash and stabilise opex. In the case of Wind, this will mean an opportunity to reduce debt, which at group level at Vimpelcom currently stands at €27.7 billion gross, and meet the capital requirements for LTE roll-out in Italy.

The Italian market

Italian mobile market penetration currently stands at around 158%, one of the highest rates of penetration in Europe. Wind is Italy’s third largest operator with 24% of market share behind TIM (35%), Vodafone (31%) and ahead of 3 (10%).

The LTE rollout in Italy is currently well underway with TIM rolling out 4G+ in 60 cities and Vodafone in 80 cities nationwide. The network requirement of LTE rollout is currently estimated at around 7,000 towers and there is considerable overlap of existing coverage by several Italian operators. Although TIM and Vodafone did agree to passive infrastructure sharing in rural areas (populations <35,000) and for new 4G tower builds, their agreement doesn’t extend to the country’s most populated areas and tower sharing in Italy currently stands at under 20%.

In a mature market where network coverage no longer offers significant competitive advantage and efficiencies can be found in co-location for LTE rollout, operators can gain significantly from a substantial towerco presence in order to consolidate their networks and reduce opex.

Current towerco activity in Italy

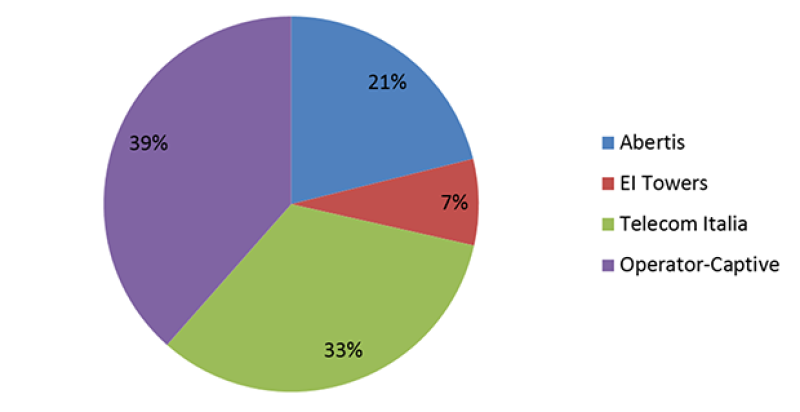

The Italian towerco market is currently dominated by EI Towers, controlled by Italian media giant Mediaset. EI Towers owns around 2,700 sites across Italy and, like other European towercos such as Arqiva and TDF, now offers telecoms solutions after originating in the broadcast industry.

Although the Wind deal will be the first substantial tower divestment in Italy to date, there has been rumors of aborted processes dating back as far as 2007, when Wind and 3 Italia attempted to divest a joint portfolio of 18,000 towers but failed to find buyers who would meet their valuation. As recently as 2014 TIM proposed the sale of its 12,000 Italian towers and did indeed sell 6,480 of its Brazilian towers to American Tower for $1.2 billion in a bid to reduce the company’s debt and regain an investment-grade rating after being downgraded to ‘junk’ status in November 2013. Current reports suggest that TIM is now considering an IPO for their Italian tower portfolio in 2015.

Abertis already owns tower assets in Italy, having bought TowerCo from Alantia in 2014 for €94.6 million. TowerCo works with all of the country’s major MNOs including Telecom Italia, Vodafone, Wind and 3 Italia. Abertis is believed to have acquired all 306 sites managed by TowerCo, which offer coverage for over 3,000km of toll road in Italy including 212 towers and 94 points in tunnels.

Adding the 7,377 Wind towers to their portfolio will increase Abertis’ footprint and make them the largest towerco in Italy by a considerable margin. Taking into account reports of Telecom Italia’s tower portfolio standing at around 12,000, EI Towers’ at 2700, and estimating that the remaining operator-captive towers will number around 14,000, Abertis’ new combined tower portfolio of 7683 will represent around 20% of the total number of towers in Italy.

Comparison with the broader European tower market to date

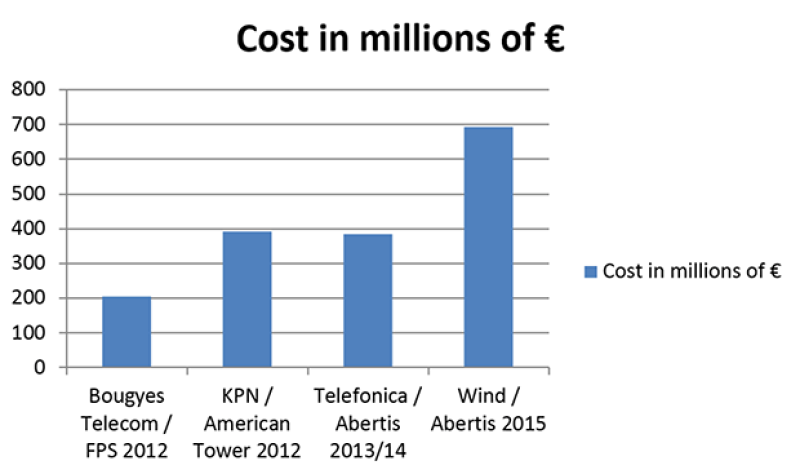

Over the last three years the European tower market has seen several deals of substantial scale involving the transfer of assets from mobile network operators to independent towercos, most notably the Bougyes Telecom deal with FPS in 2012, KPN’s German operator E-Plus and American Tower in 2012 and most recently the transfer of Telefonica’s Spanish tower portfolio to Abertis in 2014.

When viewed as a set, it’s clear that Europe’s largest (1,000+ towers and excluding carve-outs) transactions are increasing in scale, indicating that not only is the market more able to attract and deploy the capital to transfer larger portfolios, but also that operators are willing to commit more established assets and no longer view their networks as a critical competitive advantage.

When assessed alongside the cost of each transaction, however, the resulting cost per tower is much more variable, indicating that there is no ‘one size fits all’ approach for the European tower market and that variables such as leaseback rates, tenancy ratios, tower condition and location play an important a role.

Total cost of transaction