During the past couple of decades, tower operating companies (towercos) have moved from being a few, largely national operations to a wider proliferation of well-established national and multinational businesses in many countries around the world. In the process, existing towercos have grown, new towercos have been established, some towercos have consolidated and various Mobile Network Operators (MNOs) have divested their passive site assets.

The changing landscape

Historically towercos were centred on developed countries. Since the late-2000’s, growth has particularly been driven in Asia, Africa and South America, in part as MNOs look to benefit from the capex and opex savings that a towerco can deliver, as well as the cash injection that can result from the sale of their sites. These are significant enablers for an MNO, allowing them to fund network development and new technology deployment, and to grow market size and share. Less focus on coverage as a differentiator has also been a key facilitator, as individual networks cover ever higher levels of population and differences in coverage reduce (for example, over 75% of the sub-Sarahan population in Africa now has mobile coverage).

The introduction of third party towercos, offering sites to all with a focus on cost and quality (such as power availability), has also unlocked the use of shared sites (and so shared costs) in many countries.

A new business model

This change in landscape represents a significant shift in operators’ ways of implementing their networks which still remain a key element in their business. Operators are increasingly ‘letting go’ of their networks – particularly the passive infrastructure (although, in some cases, active elements are also being released) – implementing a recognition that their infrastructure is really only a means to an end (of providing service to their customers).

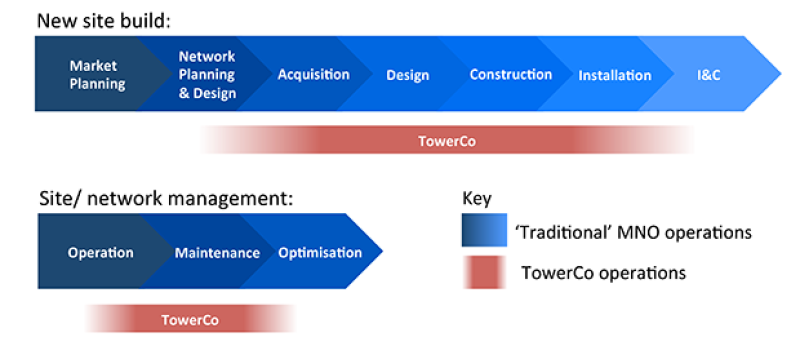

These developments are the result of the ever-wider acceptance of a business model where towercos can play an important part in the value-chain – operating and managing operators’ macro sites – see Figure 1.

Figure 1: The changing site build and management value chain

Increasing costs as traffic and technology change

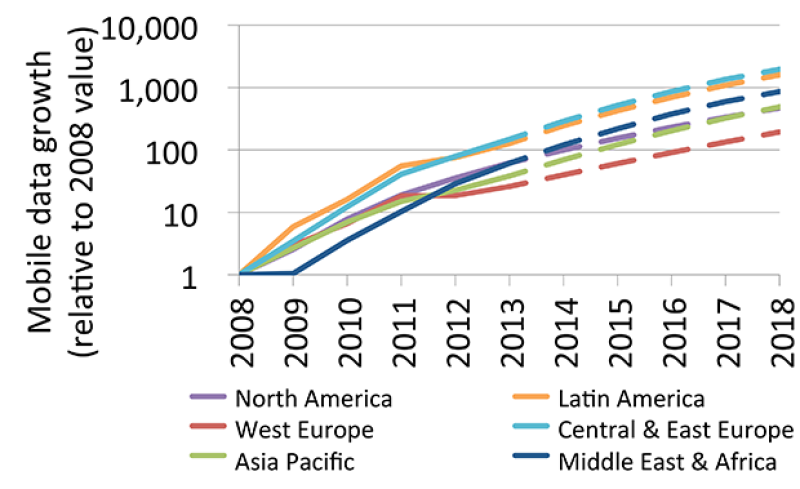

It is well accepted that a major change is underway in how mobile networks are used. Data is replacing (or, for many networks, has already replaced) voice as the dominant traffic, with data traffic growing exponentially across networks around the world, as illustrated in Figure 2.

Figure 2: Mobile data traffic growth since 2008

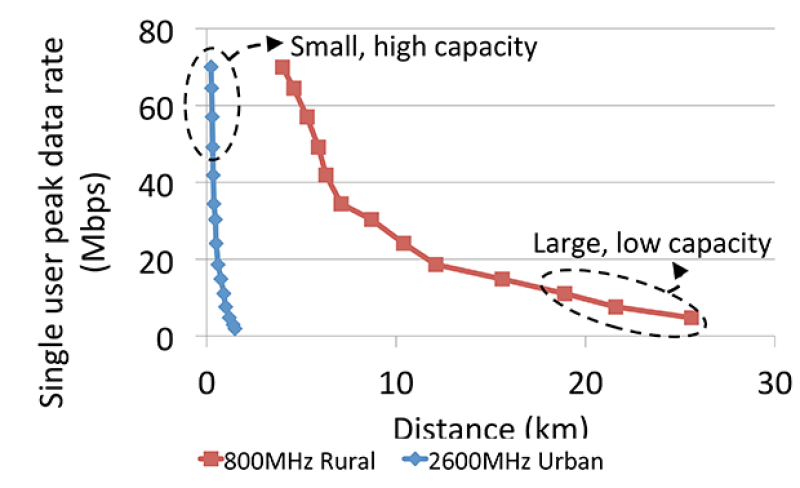

Figure 3: Trading off coverage and capacity in an LTE cell (illustrative)

And, whilst mobile operators implement ways of addressing ever increasing user demand, they also continue to push coverage out to previously ‘uneconomic’ areas – particularly rural areas, and particularly in the developing world.

This implementation of new radio technologies, deployment of small cells, and pushes into remoter regions continue to increase the cost demands placed on MNOs.

ARPU challenges and pressures on business

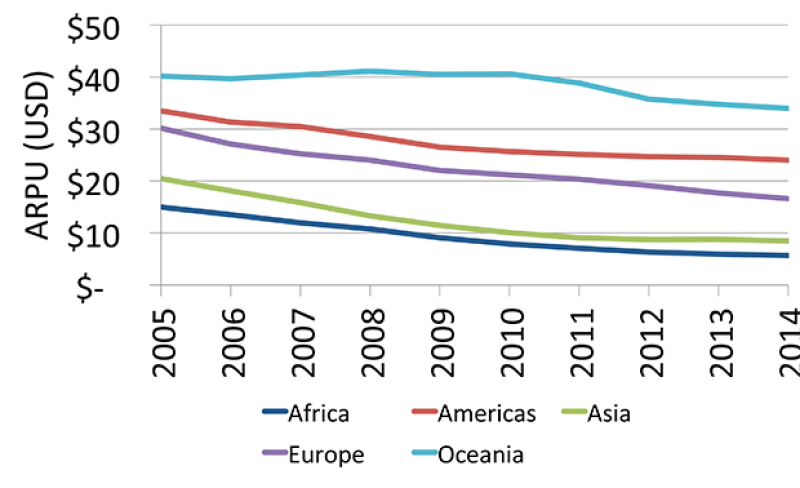

Set against this growth in data, new technology implementations, increases in coverage and (resulting) increases in costs, is the fact that, in many countries, ARPUs continue to fall. Figure 4 illustrates this across various global regions. The fall is typically driven by competitive pressures, as well as increased penetration bringing ‘lower value’ subscribers onto networks.

The regional view presented in Figure 4 does hide the fact that ARPU in a few countries has risen in recent years. For example, ARPUs in the USA have recently being rising by 1-2% pa and by up to 3% pa. in Japan. However the cost of providing the network infrastructure needed to meet increasing traffic demands is often not compensated for by any ARPU increase. And, for networks with falling ARPUs, these infrastructure cost increases are also often a second ‘whammy’ that they experience.

Rising costs and falling ARPUs place increasing pressures on MNOs – and it is these business pressures that have, in part, helped towercos flourish through the business model developments discussed above. They have encouraged MNOs to look into deeper site sharing and site consolidation – looking towards the relatively easy step of cost savings and cash injections that towercos can deliver.

Figure 4: Falling ARPU 2005-2014

The implications for a towerco

Whilst the issues of rising traffic, rising costs and falling ARPU have, in part, facilitated the establishment and development of towercos, we believe that towercos themselves must focus on these issues as they will be directly pertinent to the future shape of their businesses. And, in those terms, there are a number of actions that towercos should be considering, whilst continuing to deliver on macro sites. Some towercos have already developed and implemented strategies in these areas (to a greater or lesser degree) - however, even here, these strategies should be actively and regularly reviewed. We believe that the following three actions (amongst others) will become increasingly important to every towercos business:

1. Developing a strategy around small cells

As discussed, small cells are the future of urban capacity delivery; indeed, new macro cell deployments will ultimately reduce to very low levels (and in some countries, they already have). There will, of course, still be the need for macro coverage – and towercos can still provide this (maintaining respectable margins – particularly if they are the only source of sites in areas). However, the MNOs are, and will, increasingly focus their efforts on meeting the demands of their customers in high capacity (urban) areas – as this is where the revenue is.

Towercos should therefore continually assess the needs of their market, explore with MNOs what small cells business models could work, and develop a strategy for moving this forward – at the right time. Small cells are cost intensive (in terms of the coverage that they deliver), and towercos can carry these costs for MNOs whilst recovering them from multiple parties by delivering technology neutral infrastructure. This is already happening, in some countries and to some degree, in places such as shopping malls, stadiums, conference halls, and (to a lesser degree) outdoor city centres. Small cells will become an increasing important part of how networks move forward though, and towercos can position themselves to provide a pivotal role by building and maintaining heterogeneous networks.

2. Continually examining costs; identifying and implementing savings

The pressures on MNOs (increased costs/ falling ARPUs) have provided towercos with a significant source of business – both in increasing tenancy numbers, as well as in increasing portfolio size (through portfolio acquisitions). However these pressures won’t disappear. towercos should therefore expect MNOs to apply price pressures to them, as the MNOs will do to any of their suppliers and despite any (portfolio acquisition) agreements that currently exist. Towercos must continually examine their cost base, to see where developments can deliver savings and then work to implement these developments. For example, in the developing world power provision can be a significant part of site costs – but new power technologies can help reduce this, with expectations that future developments will further assist. Staying close to the cutting edge, and implementing new technologies, will enable towercos to maintain their financial security.

3. Developing a strategy around deeper network sharing

For a number of years, MNOs have examined deeper network sharing (beyond passive site sharing), and the associated potentially increased cost savings, but it is only relatively recently that ‘active’1 sharing has been implemented (on a wide scale within a network). If and when, this becomes more commonplace, towercos are in a good position to be a facilitator, provided that a suitable business model can be established and the prices to the MNOs are right. As a first step, towercos should look at ‘adjacencies’ – other services/areas in the business model/network provision that they could easily and reasonably move into. These could be, for example, the provision of shared site backhaul or the wholesale provision of network2 in challenging areas (as is being done by some ‘towerco’ operations in a few African countries). Beyond ‘adjacencies’, towercos must work with MNOs to understand their strategies around deeper network sharing – and be ready with considered propositions to enable them to play a significant part. Developing and implementing strategies in these areas will greatly assist a towerco in increasing their valuations beyond models centred on only site and tenancy numbers.

The implications for an MNO

There are very few MNOs globally who are not examining ways of reducing cost. And – for those that haven’t already – we believe that all MNOs should carefully examine the benefits delivered by towercos in this regard, as well as in the potential for releasing cash from their passive sites assets. It is a given that sites are only a means to the end of delivering services to subscribers (with service differentiation being the key to competition), and that towercos provide better focus on these site resources.

However MNOs should look beyond the simple cost reductions and cash injections of passive site sharing. Shared infrastructure must become central to their strategies going forward, at a macro level as well as at the small cell level. These strategies must also address deeper network sharing. However, none of these considerations are straightforward and many strategic options exist. Regulators are a significant stakeholder that must be engaged, for instance. Examining and implementing these strategic options can deliver significant benefits to the MNOs and their subscribers – and towercos can play a significant role in these strategies, if the right environment is established.

Footnotes

1 Sharing of active network antennas, feeders and electronics

2 Provision of shared towers, antennas, base stations, backhaul and switches in remote areas that interface with, and deliver traffic to, MNOs existing networks