Indonesia’s towercos represent a selection of best practice case studies combining efficient organic growth, strong MNO relationship building yielding substantial sale and leasebacks, as well as a rational rollup market for the consolidation of middle market towercos. Towercos own more than half of Indonesia’s towers, build more towers in Indonesia each year than they do in Myanmar, and have delivered solid tenancy ratio and TCF growth.

It didn’t used to be this way. As recently as 2008, Indonesia was over-populated with MNOs sub-optimally deploying capex to build parallel infrastructure – it’s a familiar emerging market telecom story. But Indonesia really isn’t an emerging market. It’s the world’s #4 mobile market, with thriving endemic industries – now including a thriving local tower industry that owns 57% of the country’s 69,458 towers, and which serves a more sustainably structured operator market led by five key players.

Some credit the start of the Indonesian tower industry success story as the 2006 regulatory policy change that enforced tower sharing. Others point to Tower Bersama’s initial transactions to ‘roll up’ passive infrastructure assets from Telenet Internusa, Bali Telekom, Mobile-8, Prima Media Selaras and SKP, soon followed by Protelindo’s landmark sale and leaseback deals with Hutchison. Whoever started it, Indonesian towercos, particularly Tower Bersama and Protelindo, became the darlings of the telecom investment community. Debt was made available and capital flowed enabling further organic and inorganic growth. Successful bond issuances and IPOs followed.

Estimated tower count for Indonesia

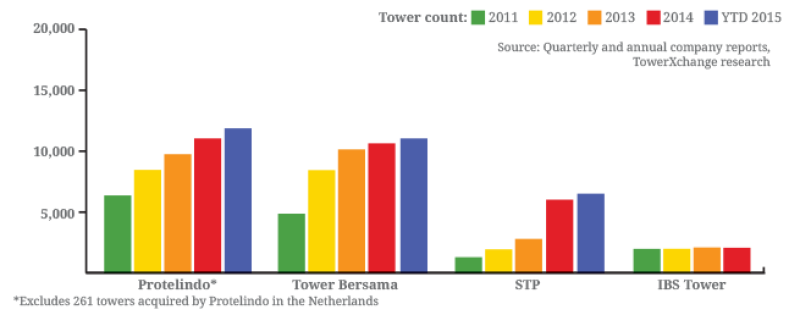

The ebb and flow of sale and leaseback deals since 2008 has led to Tower Bersama, Protelindo and STP deploying around US$2bn to acquire 12,220 towers from Indonesia’s operators, and they’ve built a similar number of build-to-suit and build-to-fill sites over that period.

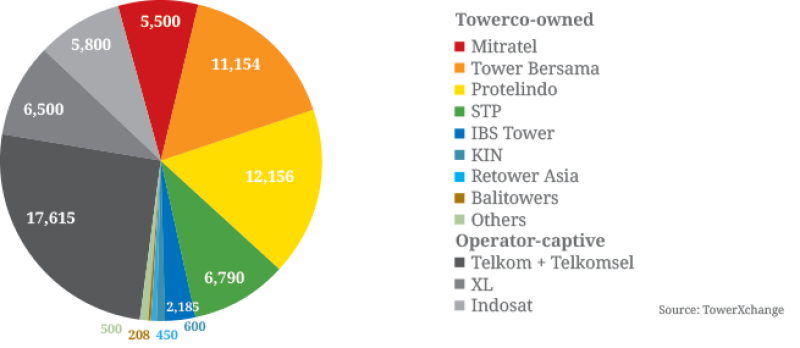

Tower Bersama’s innovative share swap acquisition of Mitratel now stands cancelled, owners Telkom having terminated the deal at the behest of the commissioner. The future of Mitratel and their 5,500 towers remains uncertain. As a result Protelindo is still the market leader with 12,156 towers, Tower Bersama is a close second 11,154 towers, and STP consolidated their position as #3 with 6,790 towers. Indonesia is host to a ‘long tail’ of diverse tower businesses, foremost of which include IBS Tower with 2,185 sites, Retower with 450, and innovative newcomers KIN with 600 towers. KIN is still flush with a capital injection from telecom and towerco thoroughbred PE-firm Providence Equity and fuelled by a strategy to roll-up selected small local towercos, of which Indonesia has dozens.

Tower deals in Indonesia 2008-2014

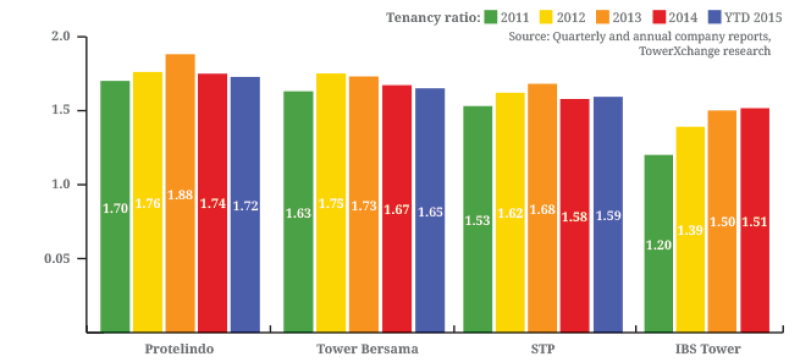

Indonesian towercos’ EBITDA and tenancy ratios have long been admired. While tenancy ratios may have temporarily stabilised at 1.7-1.8, co-locations are being added – it’s just that Indonesian towercos are building new and acquiring less mature inventory which suppresses topline tenancy ratio growth. Tenancy ratios over 2.5 remain achievable in the long term.

For now at least, Indonesia’s towercos remain unencumbered by the complexities of energy management; even though, according to Wellington Capital Advisory’s David Burke, around 25% of Indonesia’s cell sites are off-grid and another 15% on unreliable grids, power is a pass through, and Indonesia’s largest towercos are currently concentrated in areas where the grid is more extensive.

What’s next in Indonesia?

For Indonesia’s ‘Big Three’ towercos, the prized assets are Telkom / Telkomsel’s 17,615 remaining operator-captive towers, the most pervasive network in the country, of which the operator has admitted as many as 13,000 could be sold, although there is no financial imperative to divest. With the cancellation of the Mitratel deal, it is unclear whether these assets can still be acquired or whether Mitratel is destined to continue as a captive towerco, in which case it could be a vehicle for the management of the aforementioned 13,000 Telkom towers. Meanwhile, XL Axiata has already hinted that a further 4,500 towers could be divested as the company pursues it’s ‘asset light’ strategy, and Indosat may yet consider divesting some or all of their remaining 6,500 towers.

The other major factor in the future of Indonesia will be diversification of product offerings to adapt to LTE. STP and Protelindo appear to be on the front foot in this regard with their diversification into fibre, microcells and DAS. As of September 2015, STP had a 2,454km fibre network and 384 microcell poles. Protelindo recently acquired iForte and their 450 micro cell towers, seven Hotel BTS and 700kms of fibre.

It’s difficult to forecast the future of the Indonesian tower industry because there are no readily comparable benchmark markets. Protelindo, STP and Tower Bersama learned what worked and what didn’t work in other tower markets, and they’ve created a unique and highly lucrative tower industry in a dynamic and rapidly expanding mobile market.

Growth Story for Indonesia’s big four: tower counts

Growth Story for Indonesia’s big four: tenancy ratios