Mobile Market Overview

Argentina had a population of 41.8 million people and 63.1 million mobile subscriptions (source: GSMA) at the end of 2014, giving a penetration rate of 151% - the second highest in South America, after Uruguay. Around 71% of subscribers had a pre-paid account.

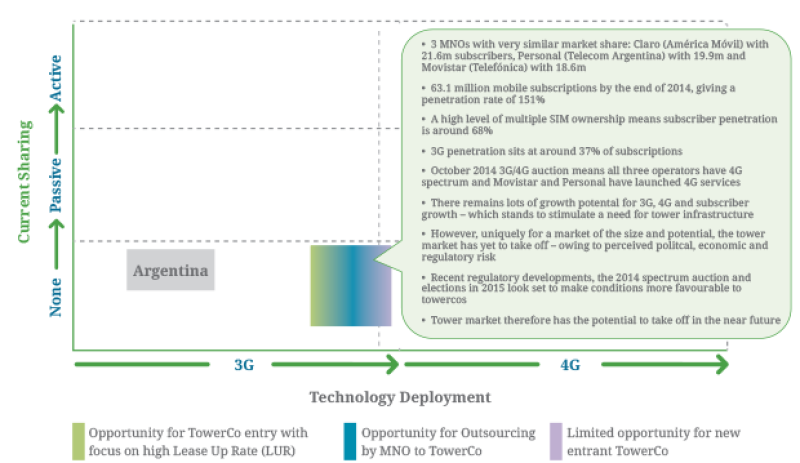

There are four Mobile Network Operators (MNOs) serving the Argentina market, with three players in close competition to be market leader (See figure 1) – Claro (América Móvil) with 21.6mn subscribers, Personal (Telecom Argentina) with 19.9mn and Movistar (Telefónica) with 18.6mn.

Key mobile developments

Argentina has one of the most developed mobile markets in Latin America, with the third highest number of subscribers after Brazil and Mexico, and the second highest degree of mobile penetration in South America after Uruguay. Whilst penetration is high, there is still thought to be potential for subscription growth, given that there is a high level of multiple-SIM ownership – meaning that the penetration rate in terms of unique subscribers sits at around 68%.

In terms of mobile technologies, Claro, Personal, and Movistar all launched 3G services in 2007, and 3G accounted for 38% of subscriptions at the end of 2014.

On October 31st 2014 Argentina’s Secretaria de Comunicaciones (SeCom) staged a multi-band spectrum auction - offering up national 4G LTE spectrum in the 700MHz and 1700MHz/2100MHz (AWS) frequency bands, as well as additional regional 3G spectrum in the 850MHz (SRMC) and 1900MHz (PCS) ranges. Winning bidders of the 4G spectrum are required to provide coverage of all locations with more than 500 inhabitants (corresponding to around 98% population coverage) within five years, with the licences valid for a period of 15 years. It is notable that, according to the GSMSA, 3G currently covers around 84% of the population. According to the World Bank, 92% of the population is urban – second only to Uruguay amongst major Latin American nations.

Figure 1: Mobile subscriptions - market share

Movistar was awarded LTE-suitable frequencies in the 1710MHz-1720MHz and 2110MHz-2120MHz bands, all of which is available for use on a nationwide basis. The company reportedly agreed to pay US$209.14mn for the spectrum. Movistar opted not to bid for 3G spectrum.

Claro won the following spectrum blocks for 3G use: 1892.5MHz-1895MHz and 1972.5MHz-1975MHz (Region I – North), 1870MHz-1875MHz and 1950MHz-1955MHz (Region II – Buenos Aires metropolitan area) and 1867.5MHz-1870MHz and 1947.5MHz-1950MHz (Region III – South). Claro was also awarded a national 4G LTE licence encompassing 1720MHz-1730MHz and 2120MHz-2130MHz. Claro reportedly paid US$281.49mn for the 3G and 4G-suitable spectrum.

Personal won the following spectrum for 3G use: 1890MHz-1892.5MHz and 1970MHz-1972.5MHz (Region I – North), 830.25MHz-834MHz and 875.25MHz-879MHz (Region II – Buenos Aires metropolitan area) and 1862.5MHz-1867.5MHz and 1942.5MHz-1947.5MHz (Region III – South). Personal also won a national 4G Long Term Evolution (LTE) licence encompassing 1730MHz-1745MHz and 2130MHz-2145MHz spectrum. Personal will pay US$410.78mn for its allocations.

The spectrum awarded to the fourth and final bidder, media conglomerate Arlink (Grupo Uno), has yet to be confirmed.

Movistar is reported to have switched on 160 LTE BTSs, covering a number of cities including Buenos Aires, Mar del Plata, Carilo and Pinamar and has sold 10,000 LTE-capable smartphones since its commercial 4G launch in December last year – as well as having 250,000 older handsets in circulation which are 4G capable.

In January 2015 Personal announced that it has switched on its LTE network in two new cities, Mar del Plata and Pinamar, taking the total number of locations served to five – having launched in Buenos Aires, Cordoba and Rosario in December 2014. The operator noted that it now has 141 4G BTS in service, up from 84 at launch. Going forward, Personal expects to have 200 LTE towers active by the end of Q1 2015, with a plan to cover 85% of the population within two years. Personal notes that it will spend around US$1.52bn on the deployment of 3G and 4G networks over the next 3 years, on top of the funds committed during the recent spectrum auction.

Claro has commented that its LTE rollout is progressing well, but that it does not intend to announce its commercial 4G launch until the network achieves significant coverage. A launch in 2015 is expected [source: GSA].

In terms of 4G roll-out, according to media channel Clarin, by mid-January 2015 Movistar and Personal had around 100,000 4G users between them – although Personal had previously announced that it had signed up 200,000 LTE users across its three initial launch cities. GSMA puts the figure slightly higher than Clarin – estimating that Personal had over 150,000 LTE subscribers by the end of 2014. It is perhaps too early to be confident about precise subscriber figures, with better data likely to emerge as 2015 progresses.

The tower sharing market

Perhaps uniquely for a market of its size, maturity and growth potential, Argentina’s tower infrastructure market remains completely undeveloped, with very little activity evident to date. Regional big-hitters like American Tower and SBA report no towers assets in Argentina despite having coverage in most of the other prominent markets in the region. Neither has there been much evidence of investment activity by private equity companies – which have been active in the creation of towercos in other Latin markets such as Mexico and Chile.

There are a number of potential reasons for this anomaly between the apparent potential of the market and the actual level of towerco activity. Firstly, there has been a significant degree of financial instability – with a recent currency devaluation and high levels of inflation – which represents a degree of risk. The stance of the left-wing government – including threats of nationalisation – may also have led to caution on the part of external towercos fearful their assets might be seized. There has also been a degree of regulatory and market uncertainty – for example regarding the ongoing sale of Telecom Italia’s controlling stake in Telecom Argentina – which has been dragging on for over a year. Argentina ranks 124th in the world in the World Bank’s Ease of Doing Business rankings (only Bolivia and Venezuela rank lower amongst major Latin American states) – and factors like corruption have been a problem – although this is far from unique (Brazil ranks 120th and yet has a thriving tower market).

There are also a number of reasons for believing the tide may be turning, and that the tower market in Argentina may take off in the near future.

From a regulatory perspective, for example, there were significant developments in 2014. In December Argentina’s Chamber of Deputies, the lower house of the National Congress, approved a new telecommunications law, replacing legislation dating back to 1972. The ‘Digital Argentina’ bill will allow companies to provide bundled telephone, internet and cable television services. It also creates the Autoridad de Aplicacion de las Tecnologias de la Informacion y las Comunicaciones (AFTIC), a new seven-member body responsible for controlling and regulating all ICT-related matters. Critics argue that the new bill, which still needs to be signed by President Cristina Fernandez, will benefit market leaders rather than aiding competition – and it is a little early to assess its impact on the tower market, but the move is seen as being broadly positive.

From a political and economic perspective, there is a chance that the advent of a new government following the October 2015 national elections could signal the return to a more stable business friendly environment.

From a mobile market perspective, the recent spectrum auctions and demand for 4G services mean that there will be a significant need for additional tower infrastructure if the operators are to meet the coverage targets imposed as part of their licence conditions.

Conclusions

The Argentina market has many positive characteristics with regard to its potential for towercos – with three sizeable, competitive mobile operators vying for leadership, high penetration yet potential for subscriber growth, and a nascent 4G mobile market. Significant tower infrastructure will be required to meet coverage targets and to cater for mobile data date demand in large population centres – with operators likely to be keen to share infrastructure to protect returns. Given the lack of towerco activity to date, the market also represents something of a unique greenfield site, which the leading international players and investment houses are likely to be eying with a view to making first move.

It is less a question of “if” and more of “when” will be the right time to make that move. Given recent regulatory and 4G developments the answer is likely to be sooner rather than later – with an expectation that there will be start to be announcements regarding tower activity as 2015 unfolds.