BMI View, by Amy Cameron, MEA ICT Analyst: Low ARPUs and a large rural population are key factors driving the development of Tanzania’s towers market. Although these circumstances have put a drag on subscriptions growth in recent years, Tanzania’s very bright economic growth outlook combined with the positive impact of falling oil prices could yet accelerate the pace of growth in the mobile market, and increase demand for towers infrastructure.

Tower sharing already the norm

Tanzania is already one of the most developed third-party towers markets in Sub-Saharan Africa. Millicom-owned Tigo was the first operator to offload its portfolio of 1,020 towers to a joint venture with Helios Towers Africa (HTA) in 2011. In 2013, mobile market leader Vodacom followed suit and sold 1,149 towers to Helios Towers Tanzania, in the 2011 joint venture. In November 2014, it was confirmed that Airtel’s sale of 3,100 towers to HTA earlier in the year included its portfolio of approximately 1,000 towers in Tanzania. Although smaller operators Zantel, owned by the UAE’s Etisalat, state-owned TTCL and Benson still retain their tower assets, TowerXchange estimates that Helios Towers Tanzania controls just under 80% of all mobile tower infrastructure in the country. Through its partnerships with Vodacom, Airtel and Tigo, it also manages infrastructure for more than 93% of all mobile subscriptions, with the three operators claiming market shares of 37.2%, 31.4% and 25.1%, respectively, in September 2014.

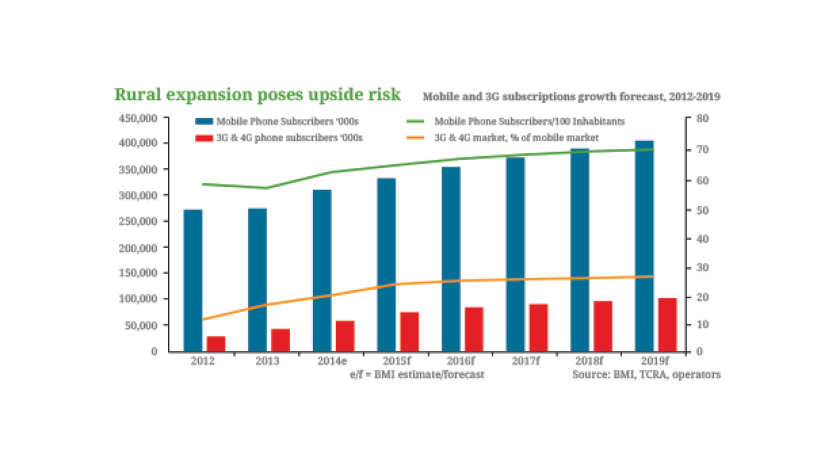

Rural expansion poses upside risk

Mobile and 3G subscriptions growth forecast, 2012-2019

Helios Towers Tanzania a crucial player in network expansion

BMI estimates that at the end of 2014, Tanzania’s mobile penetration rate was just 61%, below the regional average of around 70%, and that 3G subscriptions accounted for less than 20% of the entire mobile market. This means there remains significant room for growth in the basic voice and nascent mobile data markets, which will require expansion of mobile networks to reach underserved rural areas and tower densification in urban areas to respond to rising demand for mobile data services.

However, BMI currently forecasts underwhelming subscriptions growth in the mobile market. Tanzania’s ARPUs fell sharply during the price wars that swept across the region, dropping from more than US$7 in 2008 to US$3 by 2011. These partially recovered as Vodacom, Tigo and Airtel collectively raised tariffs during 2012 and 2013, but also contributed to subscriptions growth slowing nearly to a halt, with population growth outpacing mobile subscriptions growth in 2013.

Slowing growth momentum is also closely related to the fact that most subscriber acquisition opportunities lie in under- or unserved rural areas, where 72% of Tanzanians live. In order to overcome stagnation in the mobile market, operators must make heavy investments in expanding networks to reach these subscribers. In its fiscal year ended March 2014 Vodacom invested around US$124mn in network expansion, while Tigo announced that it had earmarked US$104mn for network expansion to rural areas in August 2014. These investments offered an important boost to subscriptions growth in the first nine months of 2014, and underpin BMI’s forecast of positive growth between 2015 and 2019.

Nevertheless, with ARPUs set to remain below the US$5 mark over the next five years, despite growing private consumption trends, BMI believes tower sharing provides the only truly sustainable solution to rural network expansion. As the only tower company in Tanzania and with a strong relationship with the three leading mobile operators, Helios Towers Tanzania will be instrumental to expanding networks to underserved areas.

A crowded market

Tanzania mobile market shares (%), September 2014

Viettel entry could catalyse consolidation

In October 2014, Vietnam-based Viettel won a concession to build and operate a 3G network in Tanzania. Viettel started building its national network in November and is expected to launch commercial mobile services in July 2015, according to Tanzania’s deputy communication, science and technology minister, January Makamba. Viettel plans to invest US$1bn in a new 3G network and to focus on rural areas, connecting around 4,000 villages currently without a telephone network to mobile services by 2016.

The addition of a new player and intensification of competition in the mobile market bode well for Helios Towers Tanzania. With urban areas already heavily penetrated, it is nearly certain that Viettel will choose to lease capacity on existing infrastructure rather than invest in building out its own. Viettel’s stated plans to direct investment towards reaching underserved rural areas confirms this view. Helios Towers Tanzania will therefore benefit from a rise in tenancy ratios in urban areas.

One consequence of Viettel’s entry that could affect the towers market is the increased likelihood of consolidation across the mobile sector. While any change to TTCL or Benson would have little tangible impact, given their combined market share of less than 1%, Zantel’s reaction to tougher competition could have a larger impact. We see three potential courses of action for Zantel. It could choose to ramp up its expansion into mainland Tanzania, which would likely include leasing capacity from Helios Towers Tanzania; it could choose to improve its fiscal position by selling off tower assets, which could open an opportunity for Helios Towers Tanzania to expand into Zantel’s stronghold in Zanzibar; or it could become an acquisition target for one of the three larger players, which would reduce the number of potential tenants for Helios in Tanzania.

Tanzania a political and economic bright spot

Aside from the presence of several major regional players and strong long term mobile growth prospects, Tanzania’s stable political environment and bright economic outlook also make it an attractive towers market. BMI forecasts Tanzania will be the fourth fastest growing economy in Sub-Saharan Africa (SSA) between 2015 and 2019, with average annual GDP growth of 7.5%. During 2015 and 2016, private consumption will be the main driver of growth, which will underpin rising demand for mobile voice and data services. Over the long term, Tanzania is set to see sustained growth as offshore gas reserves now under development come online. In terms of the political outlook, BMI expects national elections scheduled for October 2015 to be fair and relatively free of violence or major public protests, with the currently ruling Chama Cha Mapinduzi (CCM) party expected to remain in power.

But Tanzania is not immune from political risk; for example a corruption scandal in the power sector in November 2014 led the development partners group, including the World Bank, African Development Bank and several developed states, to withhold general budget support for the 2014/15 fiscal year, ending in June. This triggered an acceleration in inflation and led BMI’s Country Risk team to make a slight downward revision to our real GDP growth forecast for Tanzania in 2015.

As the November incident suggests, corruption remains a key political risk for all companies operating in Tanzania. In the towers market specifically, the area of business operations most affected by corruption issues is the import and delivery of fuel to power base stations.

Tanzania a regional outperformer

Tanzania versus SSA real GDP growth forecast, 2012-2019

Added benefits from lower oil prices

Tanzania is among the biggest beneficiaries in SSA of the collapse in Brent oil prices from more than US$100/bbl to US$60/bbl in the second half of 2014, and to US$50/bbl in early 2015. During the 12 months to September 2014, oil accounted for 35.6% of all goods imports to Tanzania. The sharp drop in oil prices, which BMI’s Oil and Gas team forecast to remain subdued during 2015, and range between US$60-70/bbl over the five years to 2019, led Tanzania’s government to cut the maximum retail price for a litre of petrol by 6.8%, diesel by 5.9% and kerosene by 7.2% in late 2014.

This will benefit the towers market in two major ways. First, lower import costs for Tanzania will help curb inflation. The combined impact of lower household energy costs and reduced inflation will offer a boost to private consumption - a metric which is closely tied to usage of telecoms services.

Meanwhile, in areas outside the reach of the power grid, telecom and tower operators remain heavily reliant on diesel generators to power mobile base stations. Lower energy costs will therefore help to reduce HTA’s operating costs and, in turn, operators’ tenancy costs in Tanzania.

www.businessmonitor.com/bmo