2014 was the year the SSA independent tower industry reached scale. Africa’s ‘Big Four’ towercos each have tower counts over or approaching 10,000 assets. Having diversified country and counterparty risk and grown portfolios to the point where best practices can be shared and economies of scale realised, the prevailing opinion at the Q4 2014 TowerXchange Meetup Africa seemed to be that Africa’s ‘Big Four’ towercos were moving from land-grab to a period of integration of assets, driving toward profitability and prospective IPO / trade sale in 18-36 months time.

One of the main reasons the land grab is coming to an end, although not yet complete, is that the investibility of emerging market towercos is somewhat dependent on the credit worthiness of the anchor tenant. Thus the ‘Big Four’ towercos don’t want all SSA’s towers – especially as many are in overlapping locations. Independent towercos currently own 47,600, around 29% of Africa’s towers. The addressable market may be a little under 100,000 towers, perhaps 55% of the current tower count.

Airtel and MTN in brief

As we’ve seen in the two previous analyses, the tower monetisation strategies of Africa’s two largest MNOs is almost complete – Airtel will have no towers left to sell by H2 2015; MTN has sold towers in five of it’s top six markets, with only its coveted South African towers and a few high risk countries from MTN’s small opco cluster remaining operator captive.

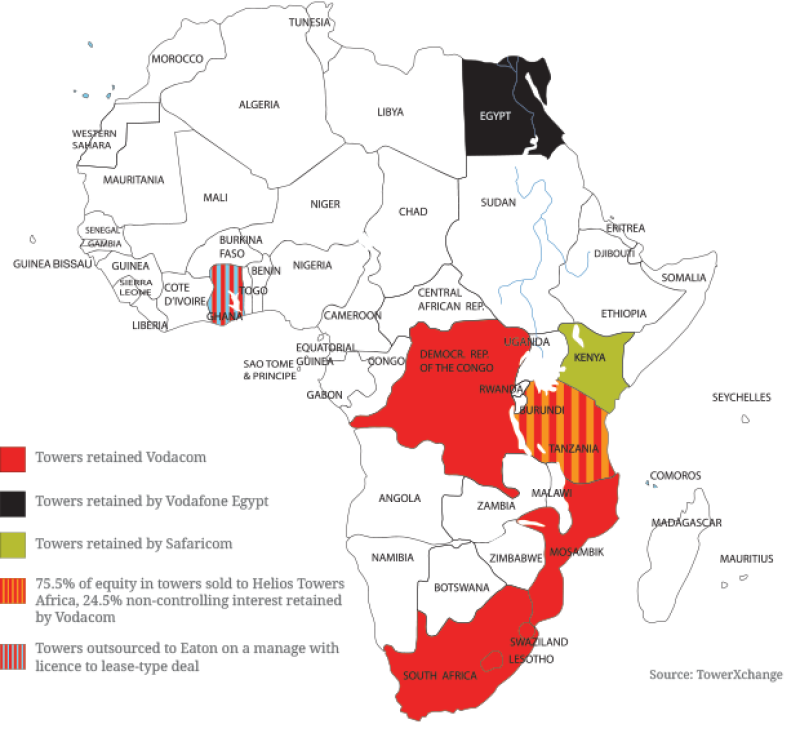

Vodacom, Vodafone and Safaricom

Apart from an early ‘manage with license to lease’ (MLL) deal in Ghana and the sale of 1,149 towers to Helios Towers Africa in 2013, Vodacom, Vodafone and Safaricom seem to consider their tower assets too strategic to divest. Nonetheless, the recent second tower transaction in DRC (Airtel’s towers following Millicom/Tigo’s in being sold to Helios Towers Africa) and the imminent MobiNil deal in Egypt might prompt re-evaluation of potential tower deals in either market.

Rumors that Safaricom might participate in a JV towerco with Airtel in Kenya have long since been forgotten – the latest rumors that Safaricom is considering starting their own towerco sound similarly incredible, although their market dominance and the relative strength of their network means a Safaricom towerco could be a lucrative venture. However, on balance TowerXchange feel status quo is the most likely future of Safaricom’s towers in the near term.

Meanwhile in Mozambique, the turbulence caused by Viettel’s aggressive network rollout and launch, coupled with the Vietnam-owned operator’s reluctance to participate in bi-lateral tower sharing, makes a Vodacom tower sale unlikely. It seems more likely that Vodacom would seek an infrastructure partner more specialised in rural connectivity in Mozambique.

While the recently commenced Telkom passive infrastructure sale RFP might stimulate a re-evaluation of Vodacom’s appetite to divest towers in South Africa, TowerXchange feel that the strength of Vodacom’s position in the market means they may be content to be late movers, if they move at all in terms of divesting towers in their South African heartland.

While Vodacom, Vodafone and Safaricom are obviously distinct entities, with Vodafone as a common shareholder, there is no imperative to raise capital. While these companies play their cards close to their chest when it comes to tower deals, don’t hold your breath for much tower transaction activity in SSA from Vodacom, Vodafone and Safaricom in 2015.

Vodacom, Vodafone and Safaricom consider most towers too strategic to sell

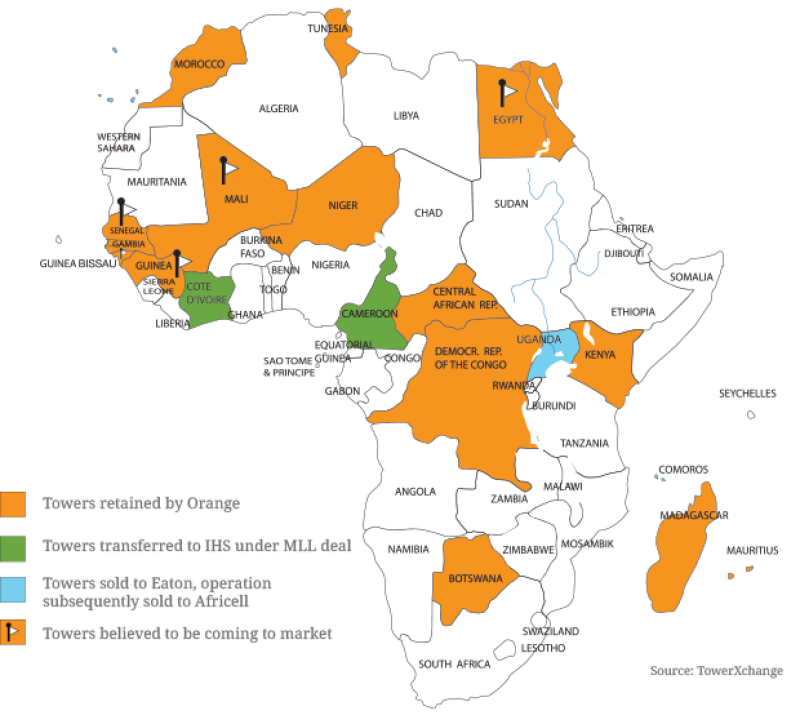

Orange

Orange has seemingly preferred MLL deals to date, as agreed in Cameroon and Cote d’Ivoire with IHS, and in Kenya with Eaton Towers before the contract was cancelled amid rumors of Orange’s impending exit from the market.

Orange has sold towers to Eaton Towers in Uganda, where Orange has since sold their operator license to Africell, while the sale of ~3,500 MobiNil towers in Egypt may close around the end of H1 2015. Orange / Sonatel is also about to commence a process to seek a partner towerco in Senegal, Mali, Guinea Bissau and Guinea Conakry.

Orange retains tower assets in several markets where towercos are increasingly active, including Niger, where Eaton are believed to be acquiring Airtel’s towers, and Madagascar, where Eaton’s potential acquisition of Airtel’s towers would place them alongside TowerCo of Madagascar, formed from the spin-out of an initial 50 Telma towers, but since grown to a tower count of over 200. While the transactions in Niger and Madagascar could accelerate any MLL or sale and leaseback (SLB) opportunity Orange considers bringing to market from those countries, we understand Orange has looked at a tower deal in DRC and feel a managed services deal structure is the most viable option.

In conclusion, Orange’s passive infrastructure sharing programme has transferred towers in several of their most attractive SSA markets, but they still retain plenty of desirable assets. Perhaps the biggest question is whether the towercos have any appetite for MLL deals now that they own 90% of their towers in SSA (up from 69% at the end of 2013)? Or whether Orange has any appetite to consider SLB deal structures in remaining markets?

Orange prefers manage with licence to lease deals

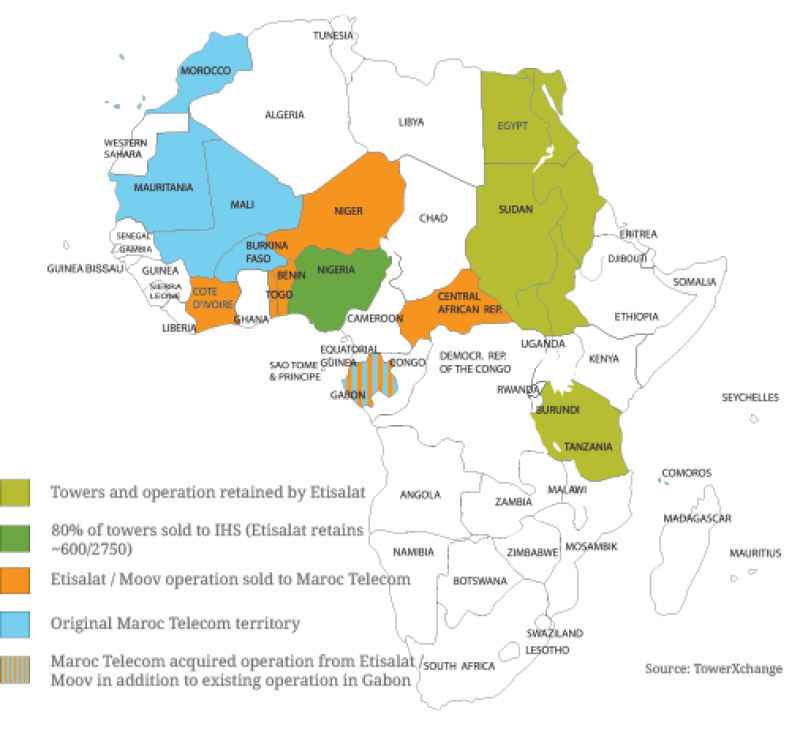

Etisalat / Maroc Telecom

We have to overlay an Etisalat and a Maroc Telecom map to track assets that changed hands when the Atlantique Telecom business was recently sold, Maroc Telecom acquiring assets in six countries for US$650mn. In parallel, Etisalat acquired Vivendi’s 53% controlling stake in Maroc Telecom for US$5.3bn.

While the dust is still settling on the restructuring at corporate level, it is notable that Maroc Telecom now operates in several markets where independent towercos are active, including Ivory Coast, where IHS owns or markets the majority of sites; Niger, where Eaton is currently setting up shop having acquired Airtel’s towers; and Gabon, where we understand Helios Towers Africa are in pole position to acquire Airtel’s towers. In addition, if and when the Orange / Sonatel process concludes, it may bring a towerco into Maroc Telecom’s Mali market. So, while Maroc Telecom has made no suggestions that they are considering tower sales, TowerXchange note that they may have opportunity to do so in 2015.

Etisalat closed their first tower deal in November 2014, selling ~80% of their Nigerian towers to IHS. Etisalat retains their towers in Sudan, Egypt and Tanzania – the towers in the latter two markets being perhaps the next most attractive to towercos. The aforementioned imminent MobiNil tower sale could inaugurate a wave of passive infrastructure consolidation in Egypt, which could provide an opportunity for Etisalat Misr to monetize their towers. However, the situation in Tanzania is less clear, where #4 ranked operator Zantel’s Zanzibar-centric tower portfolio remain the only significant operator-captive assets in a market otherwise led by Helios Towers Tanzania, which has acquired the towers from the operators ranked #1-3. While a Zantel tower sale remains a possibility, rumors continue that Etisalat might prefer to exit Tanzania altogether.

In conclusion, there are several potential SSA tower deals within the Etisalat-Maroc Telecom axis, but TowerXchange don’t think any are imminent.

Etisalat sells selected towers to IHS, operations to Maroc Telecom

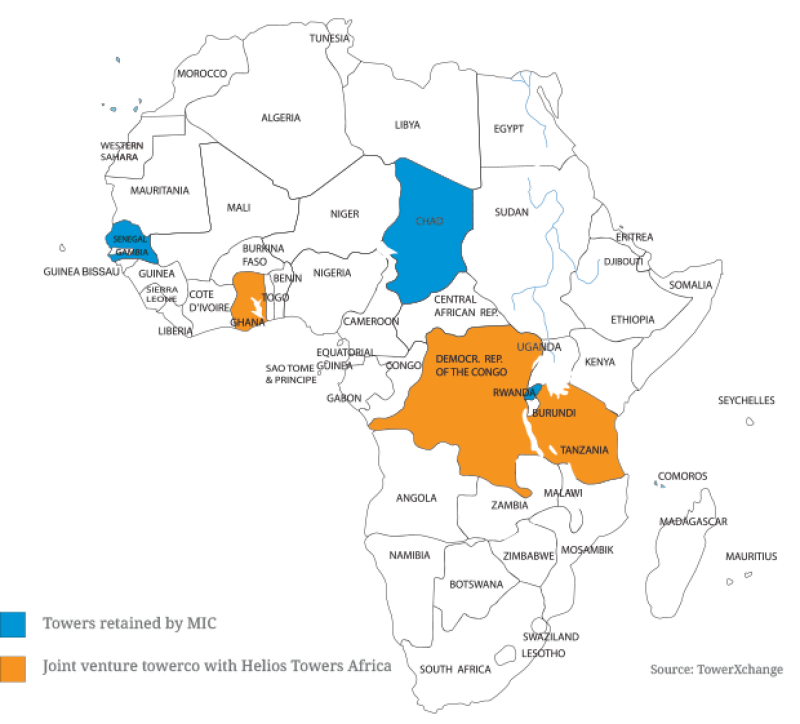

Millicom / Tigo

Millicom / Tigo undertook the first pioneering tower transactions with Helios Towers Africa in Ghana, DRC and Tanzania from 2010-11, but the group hasn’t done a SSA tower deal since.

Could the entrance of Millicom’s previous towerco counterparty, Helios Towers Africa, into Chad persuade Millicom to divest their towers in the country? As recently as May 2014, TMT Finance initiated rumors that Helios Towers Africa were in discussions to acquire Millicom’s ~800 towers in Chad. Blending the Millicom towers with Airtel’s would give Helios Towers Africa a strong market position in Chad, and create economies of scale.

With IHS acquiring #1 and #2 ranked operators MTN and Airtel’s towers in Rwanda, if Millicom is ever going to part with their Rwandan towers, it’s going to be sooner rather than later. Similarly, could the current Sonatel / Orange process in Senegal trigger a follow up tower sale by Millicom in Senegal?

With the exception of their assets in Gambia, Millicom now has an obvious and closing window to divest towers in their remaining SSA territories. While it has been rumored that Helios Towers Africa has a Right Of First Refusal agreement on all Millicom’s SSA towers, it would be surprising to see Chuck Green’s team roll into the IHS stronghold that is Rwanda – but if such an ROFR did exist, it could be leveraged in Senegal and incentivise Helios Towers Africa to take a close look at those Sonatel / Orange assets – particularly if they were available on a sale and leaseback basis.

In conclusion, we don’t think Millicom are done selling towers in SSA. A deal in Chad with Helios Towers Africa makes sense for both parties, Senegal has potential, while the question remains whether IHS would even want a third portfolio of towers in Rwanda, where IHS already have a very strong market position.

Could Millicom / Tigo return to the negotiating table?

Beyond the usual suspects

It’s oversimplifying matters to say that there are no credit worthy anchor tenants beyond Africa’s six “tier one” MNOs. Cell C were able to consummate the first major SSA tower deal as long ago as 2010 – Telkom will be hoping that has set a precedent for their current passive infrastructure RFP. Companies like Africell are doing very well in some markets, but their low-cost, rapid rollout strategies makes them more likely co-location tenants than anchor tenants – for example Africell has not built a single tower in DRC but has captured 20% market share by co-locating on 180 Helios towers.

There are interesting regional players like Econet, whose strong position in Zimbabwe means they could consider creating their own towerco. Globacom’s reluctance to part with their towers probably means they’ve missed the optimum window on a sale in Nigeria or Ghana – figure those assets to remain operator-captive indefinitely. Unitel’s passive infrastructure assets could attract a good premium if a third licence was issued in Angola – Vodacom, Airtel and MTN have all been linked with the market.

Perhaps the most aggressive new market entrant into SSA is Viettel, whose preference remains to build their own low-cost, often single tenant sites, but who seem to be warming to the principle of co-location, from their home market in Vietnam to Cameroon and, potentially, Tanzania. But again, they’re building not selling, so count Viettel as prospective co-location tenants not anchor tenants in a sale. The same applies to Smart East Africa, a subsidiary of the Aga Khan Fund for Economic Development, which is rolling out in Burundi, Tanzania and Uganda. Dig a little deeper into the market share statistics in almost any SSA country and you’ll find a layer of “non-traditional MNOs” such as urban TD-LTE plays and WiMAX operators. Such entities can contribute as much as 0.3 to prospective tenancy ratios, albeit often on shorter, discounted leases as their equipment often requires less space and less power.

So what’s still on tower companies shopping lists?

While the unprecedented SSA tower deal flow we saw in H2 2014 will doubtless slow in 2015, there are several ongoing processes which may yield further transactions in 2015.

MobiNil’s SLB in Egypt is expected to close in H1 2015

The Sonatel / Orange process will soon commence for their towers in Senegal, Mali and the Guineas

Telkom’s RFP to sell their passive infrastructure could re-ignite the SLB market in South Africa

The next wave? Airtel and Orange tower deals could trigger knock-on transactions in Burkina Faso, Chad, Congo Brazzaville, DRC, Egypt, Gabon, Mali, Niger, Rwanda and Senegal.

Could we see towercos piling into the same market as their competitors? Probably not in SSA; in what Eaton Towers’ Terry Rhodes described an “outbreak of rationality”, there has been a decreasing amount of overlap between towercos. The independent towerco business model is a natural monopoly; it works best with half as many towercos as profitable operators, suggesting most African markets can support 1-1.5 towercos, with perhaps only Nigeria and South Africa able to support two.