When the Airtel tower transaction closes, Helios Towers Africa will own around 4,500 towers in Tanzania, representing 82% of the country’s towers, and almost half their pan-African portfolio, making Tanzania the anchor of Helios Towers Africa’s portfolio. Helios Towers Africa has invested, invested and invested again in Tanzania for good reason: Tanzania is a stable, growing economy with four credit worthy tier one MNOs seeking to extend coverage into new regions, joined by an aggressive new market entrant and several niche players. Helios Towers Africa’s CEO Chuck Green was joined by Head of Projects, Innocent Mushi, in hosting a revealing round table on Tanzania at the recent TowerXchange Meetup Africa; here are some of the main talking points.

The growth of the Tanzanian tower market and of Helios Towers Tanzania

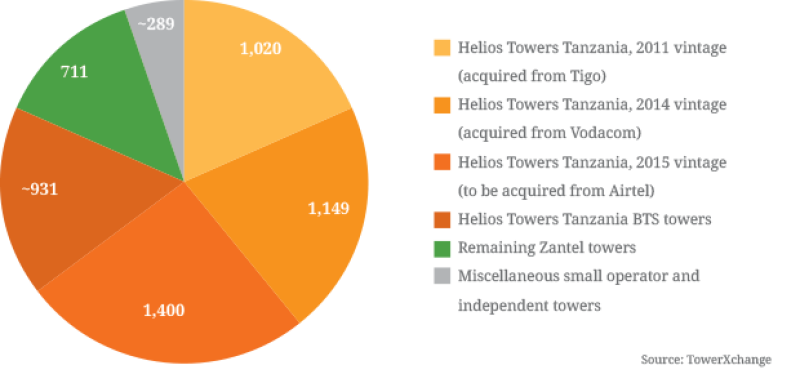

Helios Towers Africa first entered the Tanzanian market in 2011 in a transaction to acquire 1,020 towers from Millicom Tigo, bundled with Helios Towers Africa’s acquisition of Tigo’s assets in DRC. The subsequent integration of 1,149 Vodacom towers, which commenced in February 2014, is almost complete.

When Helios Towers Africa’s acquisition of around 1,400 Airtel’s towers in Tanzania closes, subject to Conditions Precedent and fair competition clearance, Helios Towers Tanzania (HTT) will own 4,500 of an estimated 5,500 towers in the country, representing more than half of Helios Towers Africa’s 8,000 asset portfolio across the continent.

While HTT’s tenancy ratio is not in the public domain, Chuck revealed that they were projecting the tenancy ratio to exceed 2.0 within five years.

Estimated tower ownership in Tanzania

Tanzania’s changing MNO market; Viettel in, Zantel out?

Helios Towers Tanzania is currently servicing significant build to suit rollout and co-location programmes from both Millicom and Vodacom, and they’ve already taken on the co-ordinates of Airtel sites to plan for additional tenants.

Tanzania’s top three operators are building aggressively in anticipation of the planned market entry and rollout by Viettel, which recently acquired a license from My Cell. Viettel had a notably disruptive influence on the Mozambique market, where their aggressive rollout of 1,600 low cost towers (spending as little as US$40,000 on some sites!) in 18 months enabled the Vietnamese-owned operator to grab significant market share from incumbent operators. The fact that 82% of Tanzania’s towers will be independently owned and marketed will doubtless accelerate any new market entrant. After initial resistance to utilising independent towers, Viettel has signed a co-location agreement with IHS in Cameroon as a means of accelerating their delayed 3G launch, so there is a precedent for Viettel leveraging shared sites.

The potential impact of Viettel’s entry into Tanzania can be illustrated in comparison with another disruptive, aggressive new market entrant. Africell leveraged co-locations on 180 Helios Towers Africa sites in DRC to grab 20% market share in 12-18 months. The market entry of either Africell or Viettel tend to engender a new world order – driving down tariffs and ARPU – indeed, Viettel is talking about rolling out as many as 8,000 sites in two years in Tanzania, a great opportunity for HTT.

Further market restructuring may follow in Tanzania, with Zantel believed to be for sale. Particularly strong in Zanzibar, the Etisalat-majority owned operator could be a ripe target for in-market consolidation.

Tanzania remains an ideal market for the independent towerco model. With a population of 40mn spread across a land mass the size of France, four strong operators and a fifth entering, none of which has dominant market share, and each with distinct regional biases, Tanzania still has relatively low penetration, so there is a lot of growth potential. Helios Towers Africa describe the regulatory environment created by Tanzania’s TCRA as “super-supportive” to infrastructure sharing – indeed the regulator’s concern about the proliferation of towers may draw Viettel into closer co-operation with HTT.

The attractiveness of Tanzania to towercos is illustrated by the fact that Tigo’s initial auction in 2011 attracted three just bidders, whereas the Vodacom process in 2013 attracted twelve.

Helios Towers Tanzania’s operational priorities

While HTT boasts a strong and motivated team, they are always seeking ways to be smarter, better and faster operationally. The company is no longer in the aggressive land-grab cycle of the business (not that they’ve necessarily finished buying assets), but is instead rebalancing their time, effort and energy into improving operations to deliver against SLAs and KPIs. Ensuring projects come in on time, on budget, and getting maintenance contractors performing as they should be are near-term priorities. As Chuck Green put it, “a dollar saved in opex or freed GLA (Gross Leasable Area) is just as valuable as a dollar of incremental tenant lease revenue.”

Green went on to describe HTT’s operational priorities as “blocking and tackling;” conducting an intelligent audit of all their own operational, mapping them, and ensuring best practices are followed.

Energy efficiency

HTT’s DC load per site peaks at 2.5-3kW per tenant, with the actual load around 1.5kW per tenant.

Tanzania’s electricity grid is one of the more reliable in Africa, with an average of 20 hours of availability, and over 70% of cell sites connected to the grid. Where feasible, connecting off-grid sites to the grid delivers better RoI than any other power investment.

HTT’s objective remains to deliver a lower cost structure, for example by leveraging energy saving solutions that make economic sense, that are “fit for Africa”, and that can be managed and maintained by the existing team in the field.

HTT is looking for the easiest way to reduce DG runtime, for example by migrating from standard batteries to CDC batteries. HTT uses a systematic process to drive down DG runtime with different solutions to meet the needs of different sites; while four strings of batteries are right for some, others might need two or six. Battery theft remains a challenge; HTT have tried welding a bar across four strings of batteries as a deterrent, and they’ve taken out insurance to mitigate the risk of battery theft, but it’s not cheap!

Opportunistic and administrative theft of batteries and fuel cannot be eliminated entirely, but towercos feel they can improve upon the levels of pilferage affecting MNOs. It comes down to visibility and proper procedures, processes and controls. People have to be appropriately motivated – employees in the refueling supply chain have to be paid a salary to compete with the temptation to take money from thieves.

HTT have some solar sites; half a dozen acquired from Vodacom, plus two or three more from Tigo. As PV prices come down, and innovations reduce the space requirement, HTT have an open mind about renewables. Chuck Green suggested: “I’m not wedded to any technology – I just want solutions that work in Africa.”

One of the challenges for hybrid energy is that there is no way to optimise hybrid power without visibility; visibility into the impact of the number of battery strings, the quality of grid, the number of tenants et cetera.

Towercos need first line data from RMS to optimise hybrid energy, and the search for a reliable remote monitoring capability is ongoing, with multiple different solutions being piloted by Helios Towers Africa. Many challenges have been encountered by all the African towercos, each of which is seeking to make RMS work; from connectivity and communications, reporting and reliability, to the difficulty of maintaining and updating systems. Many RMS are found not fit for purpose as the skill levels in the field are not on a par with the technology adopted, while the challenges of enforcing new systems and processes if any party finds RMS undesirable have been noted previously.

“We’re crawling before we can walk,” concluded Green, “if we can knock three or four hours of DG runtime out, we’re almost free of generators – then there’s no fuel to steal.”

Motivating tenants to upgrade to low power, outdoor solutions

Gain sharing used to be a naughty word, but it was incorporated into Helios Towers Africa’s Vodacom Tanzania transaction. In this case, the operator doesn’t share in any reduction in opex that comes from HTT’s investment, but they do benefit from their own investments.

HTT currently charge a lease rate inclusive of power, with the utility meter rate averaged across tenants. RMS may provide an opportunity to meter each tenant separately.

How HTT partners with maintenance subcontractors to drive performance improvements

With senior representatives of six of HTT’s principle subcontractors participating in the round table (Camusat, MER Group, NEWL, Pivotech, QTE and Sagemcom), it was possible to have a fruitful discussion about skills development across the Tanzanian telecoms/engineering talent pool, and about maintenance best practices.

While several contractors revealed details of their training and qualification programmes, we also learned how HTT’s CEO Norman Moyo had created a Maintenance Forum, consisting of all HTT’s maintenance subcontractors, to discuss how to minimise staff turnover, how to handle troublesome technicians (“weeding out bad apples to ensure they can’t move from one company to the next”), and to share best practices to optimise alarm response performance, enabling a transition to preventative maintenance.

In Chuck Green’s words, “this is where the rubber meets the road at a company that outsources O&M. Maintenance contractors have to train people well, and understand the contractual requirements we have under SLAs. It’s not just about achieving 99.95% uptime for class A sites, it’s about fire suppressions systems, certification of equipment, and a multitude of other details. There’s a way for us to work together so that field engineers visiting a site to complete a preventative maintenance task simply take a couple of pictures, and work through a tick list of other checks. I need maintenance partners who will follow the culture and processes of what we’re trying to achieve here.”

Diversification into fibre, small cells and DAS?

At every TowerXchange Meetup, the towercos are asked if they foresee the diversification of their business model from towers into fibre, and the answer is usually the same; never say never, but we have a lot on our plate at the moment and remain focused on squeezing as much value from towers as possible.

In theory, towercos are interested in anything shareable in the value chain. But most towercos worldwide don’t own or share transmission and backhaul. The reality is that, while microwave backhaul remains a bottleneck, many MNOs remain protective about shared transmission. Some towercos have spoken to fibrecos about potential joint ventures, but it hasn’t progressed beyond initial dialogues.

However, many towercos are getting into small cells and DAS – HTT have around 20 in-building solutions.