BMI View: The macroeconomic and telecoms industry environments in Cameroon offer a mixed bag of upside and downside risks. Investors and companies in the country’s budding towers market must thoroughly assess these risks to ensure long-term growth and the sustainability of their operations in the country.

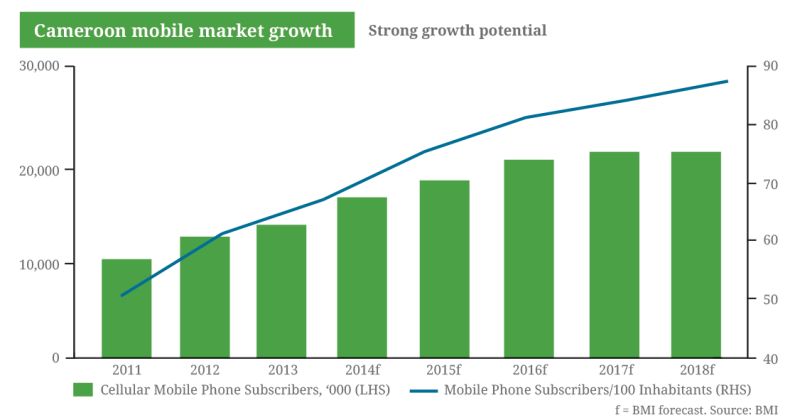

Cameroon’s mobile market is one of the least-developed in Africa in terms of market penetration and deployment of advanced data networks. The country had a mobile penetration of just 66.3% at the end of 2013, according to BMI data, and is one of a handful of major markets where a commercial 3G network service is not yet available. This scenario is expected to change over the medium term on the back of ongoing potential developments in the telecoms industry, notably the imminent launch of commercial services by the country’s third mobile licensee, Viettel. In August 2014, the Vietnam-based company announced plans to rebrand its Cameroonian unit to Nextel and launch commercial operations on the network on September 18. The move will break the MTN-Orange duopoly and drive competition-based growth in the mobile market.

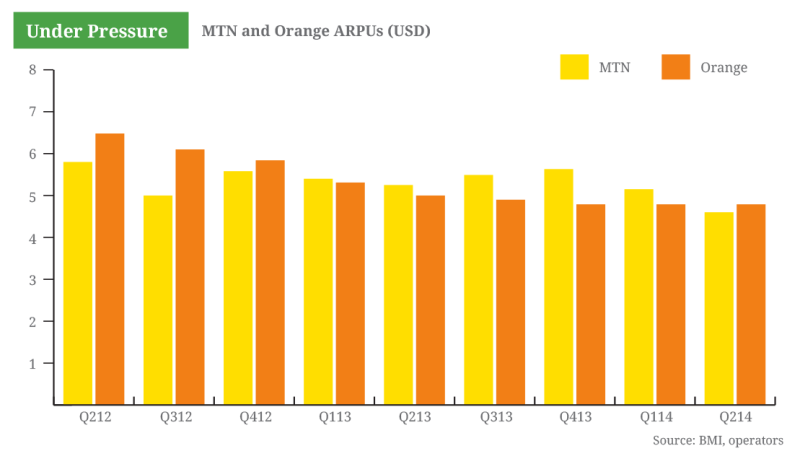

The market is already experiencing the impact of increased competition, as evidenced by operational performances in during the first six months of 2014. Incumbent operators MTN and Orange recorded combined subscription net additions of 1.632mn in H114, or average quarterly growth of 5.4%, compared to 1.639mn in FY13, or average quarterly growth of 2.3%. We attribute the strong performance in H114 to promotional activities and price offers by MTN and Orange in a bid to shore up their subscriber bases in anticipation of Viettel’s arrival. This view is supported by the sharp decline of the operators’ ARPU during the same period.

Increased competition in Cameroon’s mobile market will accelerate subscriptions growth by stimulating competitive service pricing and network expansion to underserved areas. This poses a significant upside risk to our current five-year growth forecast which expects total net addition of just over 7.1mn lines in the period 2014-2018, taking the market penetration rate to 86.8%. This outlook is arguably one of the biggest drivers of tower infrastructure outsourcing services. The operators are keen to extend network coverage to underserved areas where nearly half of the population live, but will prefer to do so in a cost effective manner considering the increasing downward pressure on mobile ARPUs. BMI calculates that market weighted average ARPU dropped below US$5 in H114, and will likely remain subdued over our forecast period.

Viettel has not disclosed its operational strategy, but we expect tower sharing and co-location to feature prominently. The company is open about its plan to implement a low-margin strategy in order to gain a foothold in the market. Viettel recorded remarkable success with this strategy in Mozambique, where it launched commercial operations in May 2012 and reported a subscriber base of more than 3mn by the end of December 2013, despite intense competition from state-owned mCell and South Africa’s Vodacom. Tower sharing will help Viettel maintain a competitive cost profile, considering that ARPUs have fallen below US$5, as well as accelerate network coverage across the country.

Viettel obtained exclusive rights 3G services until the end of December 2014, although the operator is requesting a two-year extension to compensate for the delayed launch of commercial services. It is unlikely that Viettel will have its request granted, given strong opposition from incumbent operators and other stakeholders including phone users. In February, MTN Cameroon announced plans to invest XAF600bn (US$1.25bn) in its mobile network over the next three years, on the condition that the government issues it with a 3G licence. Orange has also made extensive preparations towards the roll out of 3G services and a number of the country’s WiMAX operators, including YooMee, are making efforts to transition to 4G LTE. Competition in the 3G market and deployment of other wireless broadband technologies will require capacity enhancement and densification, and strengthen the case for tower sharing.

Mixed country risk outlook

IHS Towers has monopoly of Cameroon’s independent tower infrastructure market, having struck deals with MTN and Orange in December 2012 and April 2013 respectively. The firm is well placed to win business from Viettel, which will likely opt for the services of an established player for co-location services and, perhaps, the disposal of its tower assets as opposed to a new entrant. This makes IHS and its suppliers highly susceptible to prevailing macroeconomic and country risk factors. Presently, there is a mixed outlook for external factors capable of impacting on the operations of firms in Cameroon’s towers market. The three most salient factors, in BMI’s view, are the economic growth, political stability and security.

Positive economic growth outlook: The economic growth in Cameroon has been accelerating since 2009, and we expect that annual expansion will stabilise at around 5.0% between 2014 and 2018. Although BMI’s Country Risk team recently lowered the 2015 real GDP growth forecast from 5.2% to 4.7% to reflect the likely impact of fuel subsidy reforms on inflation and consumer spending power, we expect a recovery in 2016 when higher oil production will boost headline growth.

We also forecast real growth in private consumption spending of 5.5% in 2014 and 5.7% in 2015, driven by Cameroon’s large population and significant domestic market. Cameroon remains the largest economy in the Communauté Économique et Monétaire de l’Afrique Centrale (CEMAC), the six nation bloc with which Cameroon shares a currency, but rapid economic growth in Gabon and the Republic of the Congo (Congo- Brazzaville) will reduce Cameroon’s share of the bloc’s economy and slowly erode Douala’s position as the region’s economic hub.

Threat of political instability: For decades, Cameroon has maintained a high level of political stability, partly due to the long reign of President Paul Biya. The octogenarian has dominated Cameroonian politics since 1982, but fewer public appearances and uncertainty over his health are sparking concern among politics watchers in the country. Given that the ageing president is almost certain to leave office sometime over the coming decade, BMI believes that the country will face a difficult transition. Three possible scenarios for this change of government are highlighted below:

i. Internal power struggle - The most likely outcome, in our view, is a relatively short power struggle within the ruling party in the post-Biya era. The ruling party-dominated senate is constitutionally tasked with appointing a new president in the event of the office falling vacant. We expect that the body would succeed in appointing a consensus candidate - and that the ruling party would remain together - but warn that this could take some time.

ii. Constitutional crisis - A less likely outcome would be a constitutional crisis following President Biya’s incapacitation. The country has an unclear line of succession - the post of vice president was abolished in 1972 - and the government might struggle to appoint a new leader if President Biya were to remain alive but be unable to perform his duties.

iii. Orderly succession - The least likely route forward would be a situation in which President Biya appoints a clear successor and then moves to reduce his own involvement in government. This gradual transition of power would allow the new leader to establish his or her authority, thus ensuring stable change following President Biya’s eventual retirement or death.

Rising insecurity: Cameroon has traditionally been one of the most peaceful countries in Central Africa, but violence in two of its neighbours now threatens to destabilise the state’s frontier territories. While the religious crisis in the Central African Republic (C.A.R) appears to be subsiding, the expansion of Nigeria’s Boko Haram into Cameroon’s extreme North region has caused a wave of violence which has taken Yaoundé entirely off-guard.

We expect that Boko Haram attacks in northern Cameroon will continue, and likely increase in size and sophistication as the group recruits more local fighters. We doubt, however, that the key political and economic centres of Yaoundé and Douala face a significant threat, at least in the short- to medium-term, and expect that the economic impact of violence in the north will be limited. However, escalation that leads to attacks in Cameroon’s two key cities would be highly destabilising.

Implications for towers market players

Although strong economic growth and improving fiscal balance bode well for foreign investments and infrastructure development, one key element of growth - subsidy reforms - poses a downside risk to the towers market on the back of a potential rise in energy costs. On June 30 2014 Cameroon’s government announced that it was scrapping its expensive fuel subsidy programme, which cost the country XAF207bn (US$415mn) in 2013. We believe that the government will be forced to phase out the programme over time, with spending on fuel subsidies falling to XAF48bn in 2018. The move is already proving controversial, with reports that petrol prices increased by 14% and diesel prices by 15% in some parts of the country following the announcement.

A deterioration of the security situation would significantly raise the cost of operating in the most affected areas of the country. In Nigeria, the Boko Haram militants routinely target cellular towers to disrupt communications services. The extension of that tactic to Cameroon would have a damaging effect on the towers market, leaving tower operators and their suppliers with the options of shutting down vulnerable towers or undertake the cost providing extra security.

The political transition poses the least risk as we expect a member of the ruling party to ultimately emerge as a successor to President Biya when he leaves office. This will, to a large extent, ensure policy continuity in various sectors of the economy, including telecoms and energy.