“In 2013, we drove record levels of organic growth in both our US and international segments and added over 10,000 sites to our global asset base through the acquisitions of the GTP and NII portfolios and our ongoing site construction program,” said American Tower (AMT) Chairman, President and CEO Jim Taiclet during the conference call announcing AMT’s 2013 results. Taiclet later continued: “we have purposely and methodically expanded our asset base to over 67,000 towers that deliver strong organic growth as well as the highest margins in our industry.”

Given our focus on the tower industry in Africa, LatAm and Asia, I thought TowerXchange readers might be interested if we isolated some of the key data points relating to AMT’s international strategy.

AMT currently owns over 39,000 sites outside its domestic US market. AMT’s international segment accounted for around 25% of Operating Profit during Q4 2013, and contributed close to 40% of the total growth in EBITDA, as a function of organic growth and recent acquisitions, particularly in Brazil and Mexico.

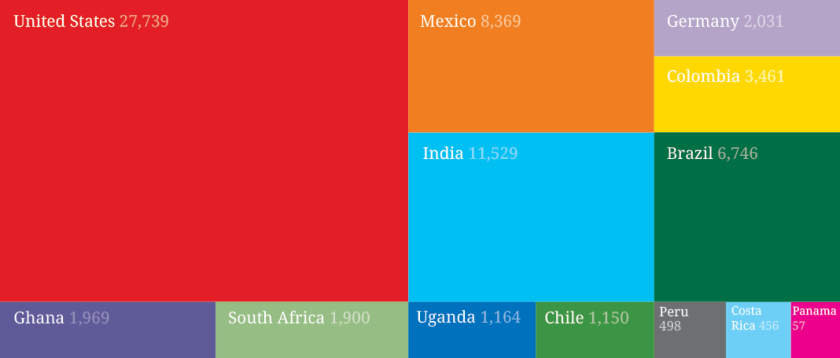

AMT International tower count as of December 31, 2013 (excludes DAS)

International tenancy ratios

AMT believes that the lower current average tenancy ratio and gross margin profile of its international portfolio combined with solid structural characteristics and attractive geographic distribution, provides an excellent opportunity for strong, sustainable long term international growth.

Tenancy ratios in selected AMT International markets

While tenancy ratios have more than doubled in Brazil since towers were acquired (see infographic), similar growth has been achieved in South Africa, where AMT reports a current tenancy ratio of over 2 tenants per site on the original portfolio they purchased from Cell C in 2011, having added over 700 co-locations to the original 1,364 site portfolio – impressive considering the acquisition included 459 rooftops.

Tom Bartlett, EVP and CFO of American Tower concluded “we believe our international operations will continue to generate organic core growth rates significantly in excess of our domestic operations. In our view, the long-term growth story in international is very exciting.”

Example tenancy ratio growth (American Tower Brazil 2002-13)

Further acquisitions

AMT prioritises international investments utilising an extensive evaluation process, including political, economic and business environment considerations. Like most towercos, they are attracted to competitive markets with three or more major carriers as prospective tenants, and where data network deployments are imminent or ongoing.

AMT understandably offer few clues as to their appetite for specific international acquisition opportunities, except to emphasise their continuing strategy to deepen their presence in “legacy markets”. This would seem consistent with unconfirmed rumours suggesting AMT’s continued appetite for opportunities in Mexico and Brazil, and AMT’s widely rumored withdrawal from interest in any portions of the Airtel Africa portfolio of 15,000 towers currently being brought to market. AMT did emphasise that “we are first and foremost having the US as a priority”.

There have recently been unsourced rumors connecting AMT with a bid to acquire Viom Networks, which operates around 42,000 towers in India.

Build to suit economics

AMT provided a rule of thumb comparison of macro site build costs of US$30k-$50k in India, US$150k-$200k in LatAm and EMEA and US$225k-$275k in the US. They spoke of the very high rates of return on build-to-suit activity, and their enthusiasm to allocate as much capital as possible to the category. CFO Tom Bartlett suggesting “if you use TCF, tower cash flow, divided by cost as a surrogate for rate of return, if you go back and you take a look at our 2009 towers that we built, we are generating 20% rate of returns on our international portfolio and over 10% on the US portfolio.” BTS activity generally comes with an anchor tenant under MLA and AMT typically looks to add another tenant within 36 months.

Conclusion

AMT is a growth stock and the company views its international portfolio as an excellent complement to its assets in the U.S. where it has created tremendous shareholder value by acquiring and upgrading key macro cell sites and leasing space to support carriers’ transition from an era of voice-centricity to the era of data-centricity. That voice to data transition is still taking place in international markets, and AMT is acquiring assets and building towers to ride this international wave of data demand growth. The need for cell site densification in International markets is illustrated by the fact that there are approximately 4,000 subscribers per cell site in Brazil, and 3,000 subscribers per cell site in South Africa, compared to 1,100 in the US.

AMT has a significant tower footprint in North and South America, including its legacy core international markets of Brazil and Mexico where it has been operating for nearly 15 years. In addition, the company has materially enhanced its presence in other regions over the last several years to solidify its position as a global player in the industry. This includes tower portfolios in India, South Africa, Ghana, Uganda and Germany, markets in various stages of wireless development where AMT sees significant opportunities for profitable growth.