TowerXchange are frequently asked for data on the US tower market, which our analyst team don’t yet cover. So we were delighted when Marc Perusat, Managing Partner of corporate finance advisory firm Xpand Capital, asked if we wanted to share some insights he’d learned about the US market in the creation of www.towerlocation.com – a unique database of cell phone and broadcast towers in the US as registered by the FCC, FAA and individual tower operators.

TowerXchange: What’s your background Marc, and what inspired you to compile a comprehensive database of US cell sites?

Marc Perusat, Managing Partner, Xpand Capital:

For the last 20 years I’ve been in TMT investment banking at Morgan Stanley and Citigroup, and in the private equity / infrastructure side with Macquarie. At Macquarie I was head of the European Communications Infrastructure Group between 2010 and 2013; in that position I was a director of Arqiva (UK tower operator), Airwave Solutions (wireless operator for UK emergency services) and Ceske Radiokomunikace (Czech tower operator).

I left Macquarie in 2013 to set up my own corporate finance advisory firm Xpand Capital, focusing on M&A deals and capital raising in the European TMT market. As I was advising a client to find US towerco partners, I realised there were no readily available sources of basic information on US-based cell and broadcast towers (numbers, location, et cetera), despite having three listed companies with a combined market cap of US$80bn (!), so I decided to create that database with the help of a few people.

TowerXchange: How many cell sites are there in the US, and how does that break down between macro towers, rooftops, DAS and other ‘special structures’?

Marc Perusat, Managing Partner, Xpand Capital:

Having aggregated the various databases into one and having updated the information in there whenever relevant, we’ve now found that the total number of towers in the US is 268,575. That figure compares with prior estimates anywhere between 100,000 to 500,000. Of these, 248,000 are active, which is a healthy 92% ratio of the total. In terms of the tower structures listed, we found that 42% of towers were guyeds, 24% were rooftops and 13% were monopole towers. DAS systems account for only 3% of the total though clearly we expect that number to grow!

TowerXchange: What proportion of the towers have been transferred from carriers to independent towercos, or were built by towercos?

Marc Perusat, Managing Partner, Xpand Capital:

It’s a bit difficult to say because the database doesn’t go back in time. Having said that, we know that wireless operators have been selling large numbers of towers in the past, especially those in rural areas that were not economical due to relatively low traffic. In terms of some of the largest deals, last year AT&T sold 9,700 towers to Crown Castle; the year before T-Mobile US sold 7,180 of its towers to Crown Castle again. In the early 2000s AT&T and Verizon had divested respectively 2,450 and 1,800 towers to American Tower.

A rough estimate is therefore that a minimum of ~8% of towers have gone from the wireless operators to the independent operators. The strange thing is that whilst they are divesting tower assets, US wireless operators are also adding to their tower portfolio as they seek to improve their networks.

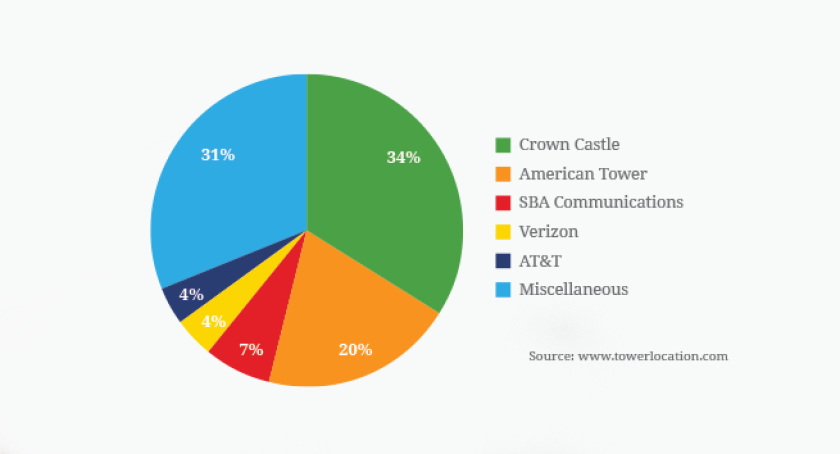

Who owns the 268,575 cell and broadcast towers in the US?

TowerXchange: How many towers do the carriers retain, and what are the prospects for further tower transactions?

Marc Perusat, Managing Partner, Xpand Capital:

Today the top four wireless operators operate 11% of all US cell / broadcast towers, a number that is surprisingly low by European standards and illustrates the fact that the independent tower operators have established a very strong foothold in that market: the top three towercos account for 61% of the total number of towers: Crown Castle is the leader with 34% of the towers, American Tower has 20% and SBA Communications 7%. Further tower transactions are expected in the US market: we know that Verizon is contemplating selling 12,000 towers in 2015. There could be others as pricing pressures in the US wireless market combined with significant LTE-related investments may force operators to seek cash from such divestments.

TowerXchange: What does the ‘long tail’ of local/regional players look like in terms of the proportion of the market they represent, and the size of portfolios in this category?

Marc Perusat, Managing Partner, Xpand Capital:

Circa 28% of the market is represented by a large number of organisations as disparate as smaller local towercos, regional carriers, TV and radio broadcasters but also federal and state agencies, railway operators, churches, et cetera. The individual portfolio sizes range from a single tower or rooftop to up to 300 towers for operators accounting for 23.5% of the total number of towers.

TowerXchange: How much growth is left in the US market in terms of tenancy ratio growth, network extension and infill sites?

Marc Perusat, Managing Partner, Xpand Capital:

There is still considerable upside ahead for US towercos. I would say that most of the growth is likely to come from network extension and infill sites. That is due to a variety of well-known factors including the search for better signal coverage, greater traffic volumes, deployment of small cells and the roll-out of high frequency networks. AT&T and Sprint alone are planning to add respectively 50,000 and 40,000 sites to their portfolio, many of which are probably going to come from existing third party sites.

Collocation ratios may increase a bit from the current 2.6x but that’s already a pretty high figure. For example, there is growth potential from specialist connectivity operators, e.g. in M2M, who may deploy their networks next to GSM operators’ own network. The downside in collocation comes in the short term from the planned decommissioning of the Clearwire, LEAP and MetroPCS networks and in the short to medium term from the potential merger of Sprint and T-Mobile.

Overall recent equity research is suggesting that the top three tower operators’ leasing revenues will grow by 6% p.a. in the next three years: still not bad by infrastructure standards!

TowerXchange: What’s your view on the potential for tower transactions and the establishment of a tower industry in Europe similar to the US?

Marc Perusat, Managing Partner, Xpand Capital:

Where there have been tower transactions in Europe, they’ve often been motivated by the need to deleverage at companies like Telefonica and Vimpelcom. Other operators such as Vodafone, Deutsche Telekom and Orange have sustainable levels of debt and therefore less need to monetise their towers. This is unlikely to remain a key driver for tower transactions.

I would expect increasing competitive pressures in the MNO market to result in further tower divestitures as MNOs are likely to recognise in due course that passive infrastructure is not core to their operations. However, they will be careful not to divest towers if it puts them at a competitive disadvantage, for example by getting locked into long term contracts with fixed price increases and limited termination rights.

The European tower industry is different to its US counterpart; specifically the independent wireless telecom tower sector is likely to remain subdued for a couple of reasons: 1) there’s some expectation of further consolidation of MNOs (and their networks) in Europe, and 2) network sharing is a lot more developed in Europe – if you’re able to co-locate on competitor’s towers, there’s less need to a third party. Still there is scope for independent towercos to thrive in rural areas. All in all, the only way I can see European independent towercos becoming dominant as per the US is if and when MNOs decide to divest the bulk of their towers.

TowerXchange: Who are the most obvious bidders for European towers? How well positioned are European towercos compared to the US towercos, particularly American Tower? For that matter, we’ve even seen Protelindo from Indonesia acquire 261 towers from KPN in the Netherlands…

Marc Perusat, Managing Partner, Xpand Capital:

Well, it depends if we’re talking about broadcast or cell phone towers. Broadcast towercos are often regulated national monopolies and as such attract infrastructure funds who put a premium on predictable cash flows. Cell phone towercos are not regulated as they operate in a typically competitive environment, therefore they attract a broader spectrum of acquirers, including other domestic towercos, infrastructure funds and international towercos, American Tower being the best example.

We’ll probably see a few European corporate champions emerging though it may take a bit of time. Abertis Telecom is the most acquisitive European towerco at the moment; they’re planning an IPO in which they would raise funds for acquisition purposes. Other European towercos have taken a less acquisitive and more domestic-focused view as the case for cross-border acquisitions is not clear-cut.

There is no doubt that US towercos could play a big role in unifying the European tower market from its current fragmented state. American Tower has already set foot in Germany and is rumoured to be looking at the Wind towers in Italy. They have the advantage of a $40bn market cap, a P/E of 50x and therefore considerable firing power! It’ll be hard for any European companies or funds to beat them… Crown Castle may join them at some point.