PT Telkom Indonesia is to acquire a stake of up to 13.7% in Tower Bersama in return for the transfer of control of it’s towerco subsidiary Mitratel, and it’s 3,928 towers, to Tower Bersama. This unique transaction represents the best example of the relatively favourable valuation multiple arbitrage between mobile network operators and towercos – at time of print Tower Bersama was trading at 3.2x it’s IPO price. The deal also puts Tower Bersama in pole position should Telkom and Telkomsel’s remaining tower assets, estimated to number 23,000, come to market subsequently.

Unique deal structure

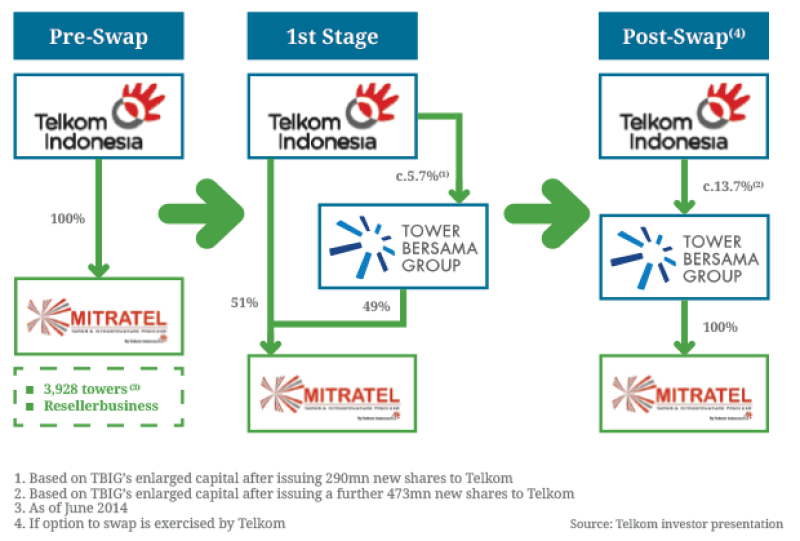

Tower Bersama (TBIG) has grown their portfolio by 35% and vaulted to the top of the Indonesian tower count table with the acquisition of Mitratel, and their 3,928 towers, from National operator PT Telkom Indonesia. The addition of Mitratel’s towers brings TBIG’s tower count to 15,195, deepens TBIG’s relationship with Telkomsel (anchor tenant on most of Mitratel’s towers), and significantly adds to the scale of the company from a revenue and geographical perspective. Mitratel’s towers are primarily located across Java and Bali, and generated revenue of ~US$130mn in 2013, and could generate ~US$70mn additional EBITDA for TBIG. Crucially, the transaction suggests TBIG would be well placed to secure an estimated 23,000 towers still retained by Telkom / Telkomsel, whose coverage outside of major metropolitan areas is believed to exceed that of their competitors in many locations, and to partner with Telkomsel in the rollout of what could be as many as 50,000 additional towers.

The first phase of the swap deal sees TBIG receive 49% of the shares in Mitratel in return for 290mn TBIG shares (approximately a 5.7% stake). No cash will change hands in the first phase of the deal, although TBIG will assume ~US$234mn of debt. The second phase could follow anytime in the next two years, during which time PT Telkom Indonesia has the right to swap its remaining 51% stake in Mitratel for an additional 473mn TBIG shares – a further 8%. This would value the deal at the equivalent of around US$904mn, including ~US$142.5mn in cash as a deferred consideration if certain performance milestones are achieved. In the meantime, TBIG will assume management control and de-consolidate Mitratel.

Analyst reaction

Analysts have come out in favour of the deal; “Despite the additional debt, the deal is credit positive for (TBIG) as it is immediately EBITDA accretive and will help (TBIG) deleverage, given the low gearing at Mitratel,” said Nidhi Dhruv, a Moody’s Assistant Vice President and Analyst, who is also Lead Analyst for TBIG. “We expect (TBIG’s) adjusted leverage (based on last twelve months EBITDA) to decline from 6.0x as at June 2014 to 4.6x for financial year 2015 and 4.1x in 2016. There is considerable scope for cost cuts at Mitratel. Mitratel’s tenancy ratio of 1.1x as of end-June 2014 is quite low compared to TBI’s tenancy ratio of 1.7x. Hence, there is potential to increase collocations and improve margins.” Nonetheless, Moody’s commentary on the deal goes on to express concern that TBIG’s “financial metrics -especially its leverage profile (remain) under pressure.”

Saham.ws stated “Including the potential cash payment, the deal is valued at EV/EBITDA of approx 10.7-12.5x (with EBITDA of approx Rp850-900bn in 2013 and assuming Mitratel can see co-lo enhancement to 1.5x EBITDA could possibly reach Rp1.1tr). This is a fair multiple, in our view.”

According to Fitch, “the all-equity deal between Telkom and (TBIG) will add about US$125mn to (TBIG’s) annual revenue and US$70mn to EBITDA. (TBIG)’s FFO-adjusted net leverage will improve to around 4.0x-4.5x from 5.0x as its annualised last-quarter run-rate EBITDA will rise to US$295mn from US$225mn, and it will consolidate additional net debt of US$225mn to its existing net debt of US$1.2bn on completion of the transaction.”

The unique structure of the transaction

How Telkom made the case for the deal

In a recent investor presentation Telkom Indonesia gave a threefold explanation for the rationale behind the transaction;

1. Increasing tenancy ratios by partnering with a leading independent towerco, in which they noted Mitratel’s tenancy ratio of 1.1 compared with Tower Bersama’s 1.7

2. Creating value in the short and long term with Telkom’s preference for a share-based consideration allowing for further upside sharing as the tower industry in Indonesia continues to grow, in which they noted TBIG’s 3.2x increase in valuation since IPO

3. Benefit for consumers, noting the government’s enthusiasm for passive infrastructure sharing to improve coverage and signal strength for consumers, in which they noted that both domestic (Indosat and XL) and international operators (Airtel, AT&T and Verizon) had recently sold towers

After almost two years of considering how best to monetise their tower assets, PT Telkom Indonesia made a smart deal, taking only a small hit to the profitability of the business due to increased tower rental costs, while securing a significant stake in one of the world’s most respected and fastest growing towercos. Critically, the independence of TBIG has been assured as Telkom Indonesia has immediately relinquished control of Mitratel and does not have a seat on TBIG’s board.

Inevitable controversy

When substantial assets change hands from a state-owned to a private company, even to a listed entity that has been one of Indonesian TMT’s greatest success stories, there is bound to be controversy, and the Telkom-TBIG deal has been no exception. And the waters have been muddied by a change in management at Telkom, where Arief Yahya has left to become Minister of Tourism.

Critics seem to have three principle complaints about the share swap; that the enlarged TBIG would have a monopolistic market share; that Telkom didn’t achieve a good return from the share swap; and that Telkom would not achieve the same long term growth in owning a minority stake in TBIG compared to owning Mitratel outright. We’ll examine the case for and against each of these objections in turn.

Critics suggesting that TBIG will secure a monopolistic market share called for the deal to be investigated by Indonesia’s Business Competition Supervisory Commission (KPPU). While the acquisition of Mitratel will make TBIG the number one towerco in Indonesia, they are unlikely to be considered in a dominant position as TBIG will own only 21.1% of Indonesia’s towers, with the number two towerco Protelindo owning 15%, and number three towerco STP growing to 9.2% after their recent deal with Axiata.

Critics have challenged whether Telkom swapping dividends and potential growth from their own towerco for a minority stake in Tower Bersama is a good deal for the state-owned company and ultimately government. Why is Telkom receiving only 13.7% of Tower Bersama in exchange for towers that constitute 26% of TBIG’s portfolio? Any knowledgeable investor in towers will tell you that the value resides more in the tenancies than in the tower count, and the Mitratel towers represent only 18% of Tower Bersama’s total tenancies. Mitratel’s tenancy ratio is 1.1, Tower Bersama’s 1.7. If one assumes a significant proportion of Mitratel towers require a degree of improvement capex to add capacity for additional tenants, and certainly one must grant that time and expertise is required to drive tenancy ratio growth, there’s logic behind a 13.7% share swap.

The loudest objections concern the relative positioning of Telkom and TBIG in relation to Telkomsel’s network extension and densification plans, which could involve building as many as 50,000 towers in the next five years. Would Telkom have been better off retaining Mitratel and selling some of it’s stock? In the end, it comes down to the usual business case of concentration on core competencies; by divesting Mitratel, Telkom is free to concentrate on selling minutes and megabytes, and they’ve secured a significant stake in an entity whose raison d’etre is to manage passive infrastructure, and who can focus on driving efficiencies within the tower network.

Telkom is swapping ownership of an immature, operator-led towerco for a stake in an independent, more proven entity, whose share price has leapt 3.2x since IPO. Again, critics might ask how much growth is left in Tower Bersama’s stock, given the maturity of the business? There remains plenty of scope for inorganic growth in the Indonesian tower market where towercos own 51% of Indonesia’s ~72,000 towers – a fully penetrated market might see towercos owning 60-70%+ of the sites, as we see in India and the USA. Indonesia needs more cell sites, and TBIG’s organic growth is well into double digit percentages. LTE will drive further growth as operators add infill sites and generate amendment revenue. While Indonesia’s first LTE service, Bolt, was launched as long ago as November 2013, the service is limited to Jakarta and surrounding cities, and Indonesia’s ‘Big Four’ operators are not expected to rollout LTE until 2015 after spectrum reallocation.

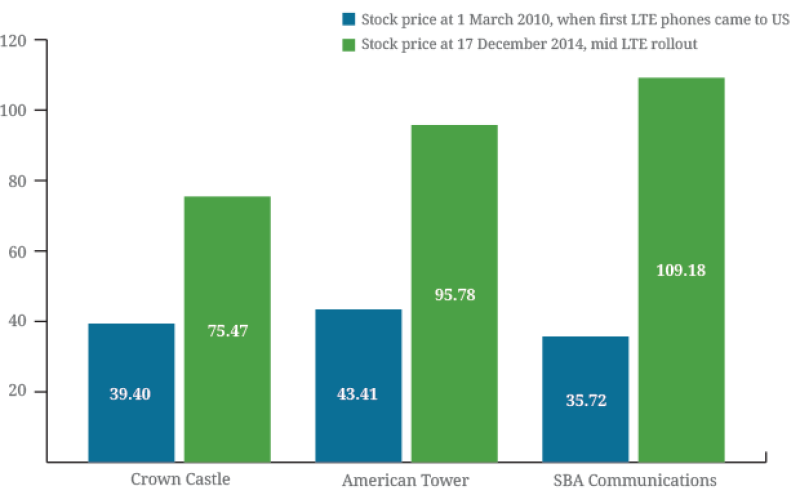

International comparisons are of limited value because every market is unique, but if one likens Indonesian towerco’s performance to date to US towercos’ performance before and after the early days of LTE in that country (MetroPCS and Verison offered the first LTE smartphones in the US in March 2010), it’s notable that US towerco valuations have risen substantially as LTE has been rolled out. It seems reasonable to forecast Indonesia’s towercos benefitting from similar improvements in their valuations.

US towerco stock prices before and after LTE

The Telkom Indonesia-TBIG deal follows hard on the heels of XL Axiata’s sale of 3,500 towers to STP for US$460mn. 51% of Indonesian towers are now owned or controlled by independent towercos, a statistic TowerXchange expect to rise in 2015 as further towers are monetised by Indonesia’s MNOs. Telkom and Telkomsel retains a further ~23,000 towers, XL Axiata still has ~6,500 and Indosat retains ~5,800. All three MNOs have a track record of divesting towers in Indonesia, and we expect further transactions, and build-to-suit contracts, to follow.

We also anticipate further consolidation among Indonesia’s “long tail” of small, regional towercos. Tower Bersama and Protelindo both have a track record of acquiring local towercos in Indonesia, but currently the most active towerco expanding by rolling up smaller portfolios is Komet Infra Nusantra (KIN), boosted by a capital injection from Providence Equity Partners, and led by CEO David Burke, widely credited as the original architect of Mitratel back when he served as EVP for Strategic Investment and Corporate Planning at Telkom.