Airtel’s long rumored sale of all 15,000 of their African towers is nearing completion. Some TMT news outlets have announced the structure of the deal but, having spoken to the CEOs of Africa’s towercos, TowerXchange can confirm that those reports are premature and that the final shape of the transaction is yet to be determined.

Figure 1: Proportion of sites on the Airtel network running 3G

Nonetheless, here’s what we do know. Airtel is prepared to sell off their 15,000 towers in digestible ‘chunks’ rather as one single portfolio. While there will be fierce competition for Airtel’s towers in proven tower markets, there may have been only one bidder in some of the less proven tower markets, giving rise to a question as to whether Airtel’s valuation will be met in each country. Certainly, as operators of ‘Africa Towers’ and shareholders in Bharti Infratel, Airtel has the expertise to retain any assets that do not attract a bid above a nominal ‘reserve price’. However, it seems likely that most of Airtel’s Africa towers will be sold.

Most commentators agree that IHS, Helios Towers Africa, Eaton Towers and Helios Towers Nigeria are all bidding for the segments of the Airtel portfolio that attract their interest, and it seems that American Tower is not participating in the process. This could be a due to a combination of Airtel wanting to shed responsibility for energy logistics while American Tower prefers a power pass through clause, or it could be a reflection of American Tower’s finite appetite for the country risk present in many of Airtel’s operating countries. It could simply be that American Tower prefers to deploy capital in the US domestic, LatAm and European markets.

Airtel has not appointed a banker adviser, but reports suggest they are handling the transaction efficiently themselves, with the process proceeding broadly in line with their ambitious target timeline – let’s put it this way, we expect to be writing an analysis of a completed Airtel tower sale in the Summer edition of the TowerXchange Journal!

Figure 2: Subscriber growth on the Airtel network

Frontier market towers

If, as rumoured, one tower company acquires the towers in the majority of countries shown in red in Figure 5, where local RAN Planners and Rollout Managers are not used to co-locations on independent towers being available, then that tower company is going to look more “frontiersy” to prospective future investors and strategic partners. Don’t misunderstand our analysis – taking on a frontiersy portfolio may not be a bad thing – we’ve often seen an exaggerated initial uptake of tenancies after the first tower transaction in a market as pent up demand for co-locations is unlocked. However, to date Africa’s towercos have only proved the efficacy of the business model in some of the more obviously attractive markets such as Nigeria, Ghana, Tanzania and South Africa, so whichever towerco acquires Airtel’s towers in their frontier markets is going to have an evangelical mission to promote the virtues of tower sharing to tenants and regulators alike.

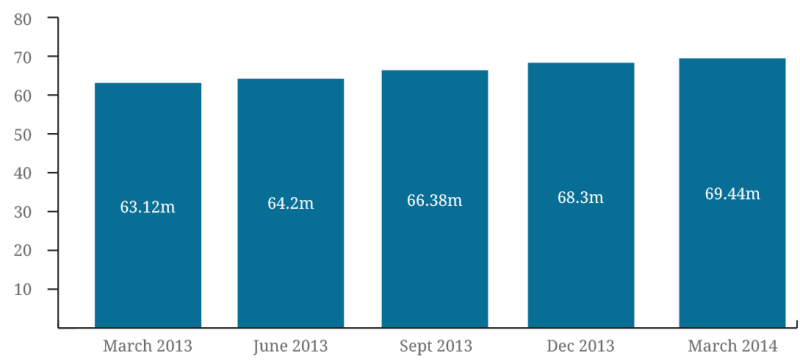

Figure 3: ARPU running through the Airtel network

While there will doubtless be many local stakeholders to win over in markets like Burkina Faso, Chad and Niger, with a rapid mobile subscriber growth from a low base and positive GDP growth, the runway for long term growth is tremendous. As we’ll see in the subsequent BMI and Mott MacDonald analyses, Airtel are not the only credit worthy tenant in these markets, but there are challenges to be overcome, not the least of which being energy logistics in countries with less than 15% electrification, and the unpredictability of regulations in a countries characterised by volatile domestic politics.

Will the Airtel transaction stimulate competition among towercos in established markets, or reinforce the market leadership of first movers?

The other side of the Airtel tower sale may attract several bidders to the process. The crown jewel in SSA African telecoms is Nigeria, which means towers assets in that country are sure to be in great demand. We’ll look more closely at the Nigerian market later in this special feature.

The sale of Airtel’s towers in Tanzania and DRC will doubtless have piqued the interest of Helios Towers Africa, which already has very successful operations in both countries, while it will be interesting to see how IHS responds to the sale of Airtel’s towers in Rwanda and Zambia, following so hard on the heels of their acquisition of all 1,269 of MTN’s towers in those countries.

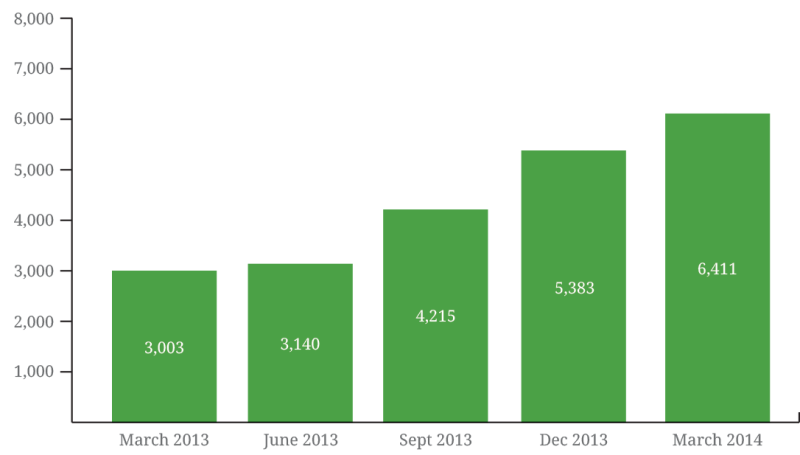

Figure 4: Exponential growth in data on Airtel’s network (data shown in millions of MB)

Exponents of the independent tower business model unsurprisingly but rightly advocate that only one or at the most two towercos should operate in any given emerging market country, in order for to creates the best opportunities to exploit economies of scale. For example, Ray O’Shea of Tanzanian O&M subcontractor NEWL explained the impact of Helios Towers Africa entering Tanzania: “where once we had dedicated teams for each operator, and field engineers spent a large proportion of their time on the road, now our model is regional, with each local team looking after a cluster of 20-25 towers for a mix of operators.”

Figure 5: Airtel ‘s towers are include countries that are both proven and unproven tower markets

Conclusion

The sale of Airtel’s African towers will redefine the landscape for Africa’s four largest PE-backed independent towercos. Some of them, probably one of them, will take on a more frontiersy character, but if the acquisition of assets in markets with significant country risk is reflected in the purchase price, it can still be a good deal. Other tower companies may have their first mover advantage in proven tower markets reinforced with supplemental acquisitions, or they may find themselves facing fierce competition.

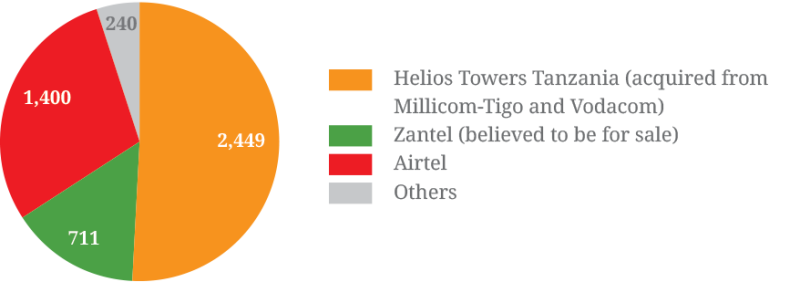

Figure 6: Estimated breakdown of the ownership of Tanzanian towers

However, TowerXchange’s main conclusion is that this is a highly investible, attractive portfolio of tower assets; it’s early days for mobile data in Africa, but the number of MBs of data running through the Airtel network has more than doubled in a year, and Airtel are a savvy and credit-worthy anchor tenant -a good business partner for towercos. The PE-backed towercos are going to emerge from the Airtel transaction significantly closer to achieving scale, so the door for new market entrant towercos to come into Africa via any method other than acquisition may be closing.