PLEASE NOTE THAT THIS ANALYSIS HAS BEEN SUPERSEDED BY THE LATEST CALA TOWER MARKET ANALYSIS HERE:

2013 was an exciting year for the Latin American telecom tower industry, with 14,035 towers divested, more than double the previous year. With 12,369 towers sold in Brazil alone, the country placed itself at the very heart of the transformation of the tower industry, also thanks to the push provided by upcoming events such as the 2014 World Cup and 2015 Summer Olympics.

With 1,666 towers divested, Mexico experienced yet another interesting year in terms of transactions while international media continue to speculate about imminent changes to the national telecom regulatory framework.

Although absent from the sale and leaseback market, Chile, Peru, Colombia and Ecuador are other countries we are keeping an eye on thanks to their push towards 4G LTE which might prompt a new wave of tower transactions in the upcoming months. Build-to-suit and middle-market towercos are active in all four countries, as well as some of LatAm’s larger towercos.

Central America and the Caribbean could be the next targets for international towercos seeking to expand their regional footprint. Some markets, such as Panama and Puerto Rico, feature many independent towers and local towercos. Others remain greenfield markets with promising macros, but lacking scale.

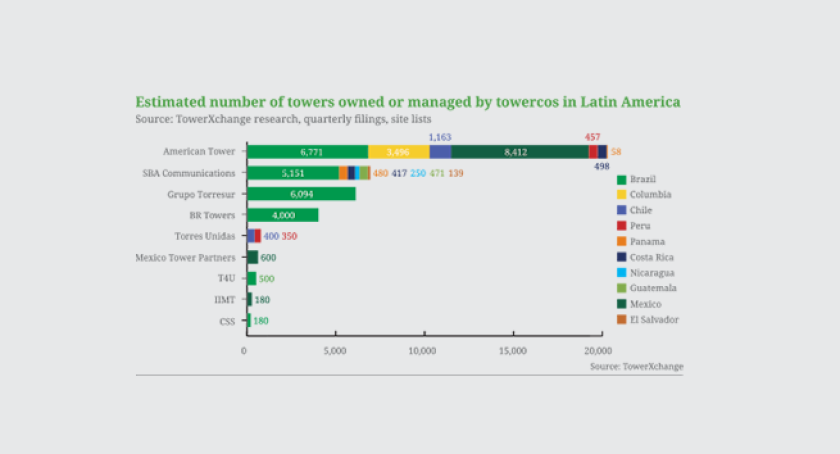

In this article we offer a comprehensive analysis of major trends, transactions and news from the LatAm telecom tower industry, starting with an updated tower count and a comprehensive report on the landscape of independent towercos active in Central and South America.

In addition to the towercos listed in the tower count graphic, TowerXchange has identified a wide array of mid-sized tower companies active in the CALA region. Brazilian focused Brazil Tower Company, QMC Telecom, Highline do Brasil and Torres Andinas are all actively pursuing BTS opportunities alongside CSS and T4U. The Mexican landscape hosts Torrecom - also active in Guatemala and Nicaragua, and Continental Tower Corp, which also operates in Guatemala, Nicaragua, Colombia, the Dominican Republic, Jamaica, Honduras, Panama, Costa Rica and El Salvador. Additionally, we report activities of Torres Andinas in Chile, Peru and Colombia as well as Torresec’s involvement in Ecuador and Puerto Rico. Teletower Dominicana is involved in the development of the Dominican Republic’s tower sector while Torres de Panama operates in Panama.

Brazil: 7,000 new towers to be built in 2014, ten active towercos and 20,000 towers on sale

The Brazilian tower market has been experiencing an unprecedented growth pattern over the course of the past three years. To quote Grupo TorreSur CEO and Chairman, Jim Eisenstein “Brazil, in particular, has been like the U.S. tower industry in fast forward.”

As previously reported, SindiTelbrasil has assessed that 9,556 new towers should be installed over the course of 2014 in order to reach the ambitious 4G coverage goal. That would mean 30 new towers per day for the entire year.

In reality, we are likely to see no more than 7,000 new towers erected in Brazil during this year and this is due both to the actual construction capacity of major service providers and towercos active in the national territory and due to the highly complicated bureaucracy behind licensing and permitting.

The proposed Law of Antennas, now in draft form, might simplify the requirements for towercos and carriers seeking permits for greenfield projects but to date, the procedure is in the hands of local governments and municipalities and hasn’t been unified.

With a wide array of mid-sized towercos such as Brazil Tower Company, QMC Telecom, T4U Tower Management, Torres Andinas and Highline do Brasil all competing to secure build-to-suit projects, the country isn’t facing a shortage of players and yet, the tower construction game hasn’t achieved the desired pace.

One additional challenge to the optimal development of the Brazilian BTS market comes from the sometimes contentious conditions - such as generous cancellation terms and heavily discounted lease rates - carriers have secured from some towercos. This has disincentivised the major international towercos from participating in the Brazilian BTS market, which could be problematic if Bloomberg are correct in their recent speculation that Brazil’s ‘middle market’ towercos had capacity to build only 1,600 towers per year. However, in light of the 60 GB of data traffic per second registered during the 2012 London Olympics and the 500 GB splashed during the US Super Bowl back in February 2012, key players in the Brazilian telecom tower sector will need to run the extra mile to meet these highly ambitious targets on time.

In the midst of this complex yet exciting scenario, American Tower, SBA Communications, BR Towers and Grupo TorreSur have dominated the Brazilian sale and leaseback market and have acquired over 20,000 towers since 2010, at an average price of US $175,000 per tower.

Brazilian tower portfolios valuations take into consideration the tower location, its existing and potential tenancy ratio, its structural capacity and the anchor tenant fee agreed with the carrier. As such, cost per tower is at best a crude measure of value.

During the recent American Tower International Analyst Day, AMT indicated that its Brazilian portfolios acquired in the early 2000s had achieved a tenancy ratio of 3.2 in 2013, indicative of sustained tenancy ratio growth of around 0.2 per year, considered very healthy for emerging market towerco economics.

To add spice to an already dynamic scenario, recent news have reported that Tim Brasil is currently considering divesting its 7,000+ tower portfolio in order to finance its 4G network plans. Rumours suggest that there might be as many as three more substantial Brazilian tower portfolios for sale in addition to TIM’s and this could bring the number of towers for sale over 20,000. We expect major towercos to gear up for an exciting rest of the year and will keep following the Brazilian tower market development as they unfold.

Mexico: low penetration rates, 111 million people and the potential to become a key telecom tower player

As stated by BMI in a recent analysis of the Mexican telecom tower sector published in the TowerXchange Journal, the next two years could prove crucial for the Mexican tower industry as various factors are contributing to create a perfect storm for investment in the country.

In 2013, Mexican President Enrique Peña Nieto issued a constitutional amend aimed at transforming the Mexican telecommunications industry. As part of the reform, a new regulatory agency was created - IFETEL - with constitutional status and a mandate to ensure economic competition and universal coverage. The new body is independent from the executive and legislative powers, unlike COFETEL, the previous acting agency.

Looking at the current status of the market, the rationale behind the reform is evident. Out of the four carriers active in Mexico, América Móvil’s Telcel, is the most powerful actor with market share beyond 70%, with the remaining market being split among Movistar, Iusacell and Nextel.

Changing the status quo in a country heavily dominated by one company is not an easy task and we will have to wait until the secondary legislation comes into place, later this year, to fully evaluate the practical impact of the reform.

In the meantime, we could witness a tremendous growth of the Mexican tower industry. It has been estimated that, in addition to the existing 22,500-23,000 Mexican towers, an additional 70,000 towers are needed in order to reach 90% coverage.

However, this might prove to be an challenging task, considering that Mexico has one of the highest costs per tower in the region. In 2013, American Tower acquired 2,790 towers for US$413 million in Brazil and 1,483 towers for US$323 million in Mexico from NII Holdings (operating as Nextel). The average price per tower in Brazil was US$148,000 whereas each Mexican tower was valued at US$252,000. And this is a consistant trend we have witnessed in Mexican transactions since 2011, when American Tower acquired 2,500 towers from Telefonica at US$200,000 per tower and Global Tower Partners bought a portfolio of 199 towers from the same carrier for US$40 million (USD 200,000/tower).

In spite of current challenges faced by the national telecom tower industry, Mexico is a country with great potential and, quoting the CEO of Digital Bridge Holdings (which owns Mexico Tower Partners), Marc Ganzi “a poster child for wireline replacement, as well as explosive wireless internet and data consumption.”

In his recent interview with TowerXchange, Marc commented: “I am particularly keen on the Mexican market, and feel we can grow our business there significantly. It can take investors quite a long time to get comfortable with the operational norms, currency, political and sovereign risks inherent in Mexico, but I’ve been there for over 15 years, which gives our investors comfort in backing us, and means we’re given the autonomy to run the business as we see fit.

There’s tremendous demand for new sites in Mexico, with significant capital being deployed by Telcel and Telefónica in their desire to cover the entire population - it’s a big country with lots of rural communities and an extremely fast growing middle class. The need for coverage and capacity sites make Mexico an ideal tower market, as it clearly will need future new builds and collocation.”

Chile: 5% 4G coverage, a proactive government and the most stable business environment in Latin America

In 2012, a new law came into effect in Chile (N. 20.599) setting clear construction guidelines in order to ensure all new towers built in the country have the structural characteristics to host multiple tenants. The same law outlined stringent conditions for the installation of towers in saturated and sensitive areas as well as compensation for communities affected by new towers’ erection.

These new rigid measurements have contributed to the apparent slowdown of the Chilean telecom tower market in spite of representing a clear push towards infrastructure sharing which has recently been mandated in rural areas.

With 4G covering just above 5% of the country, carriers are actively involved in rollout, following two successful auctions in February 2014 (700MHz 4G spectrum) and July 2012 (2.6Ghz spectrum).

The Chilean government is heavily involved in the promotion and regulation of the ICT sector and has set very clear coverage requirements that will push carriers to invest in infrastructure and expand their current portfolios by three to four times, as analysed by BMI in a recent article for the TowerXchange Journal. However, as per BMI’s report, 3G connections in Chile accounted for 26.8% of total subscriptions at the end of 2013, following growth of 29% year on year. This data shows that Chilean subscribers demand higher value services and therefore suggests that 4G is likely to capture their attention relatively quickly.

Thanks to its openness to international investment and a proactive government, the Chilean telecom industry is expected to keep delivering growth, great news for incumbent operators Claro, Movistar and Entel, and for American Tower and Torres Unidas, who both operate substantial tower portfolios in Chile.

LatAm towercos and carriers: a business partnership in the making

LatAm is host to a highly complex and thriving tower industry, led by AMT and SBA and the two Brazilian leaders, but also consisting of a host of innovative ‘middle market’ towercos supporting the region’s enormous thirst for new towers.

Although facing many challenges, especially related to the imminent need to reform telecom regulations from Mexico to Brazil to facilitate the access of new players and international investors, Central America, the Caribbean and South America are potential candidates for the further development of a profitable telecom tower industry.

With most countries over 100% subscriber penetration and with a growing middle class demanding value added services and driving demand for data, the time is right for carriers to invest in the deployment of 4G LTE and to welcome the new wave of independent towercos as a business partner enabling the sector to fully develop its potential.