Another day another deal in African towers – they’re coming thick and fast, and the pipeline of future transactions is still bulging. Today is the turn of Etisalat Nigeria, who transferred 2,136 towers to IHS Africa under a sale and leaseback deal, marking the first of several imminent major tower deals in Africa’s #1 telecoms market. In this editorial, TowerXchange CEO Kieron Osmotherly highlights pertinent details from the deal announcement, looks at the changing shape of the Nigerian tower market, and shares his commentary on the enlarged IHS.

Etisalat Nigeria announced the sale of 2,136 towers to IHS on August 7 2014, making the operator the first to market of the three major GSM operators selling their Nigerian towers. Airtel’s Nigerian towers are still on the market as part of their pan-African tower sale, although the deal is believed to have hit legal snags, while the bid deadline has passed for MTN’s prize portfolio of 9-10,000 Nigerian towers. By the end of 2014, TowerXchange forecasts that 84% of Nigeria’s towers will be owned or operated by independent towercos, with only Glo retaining their towers.

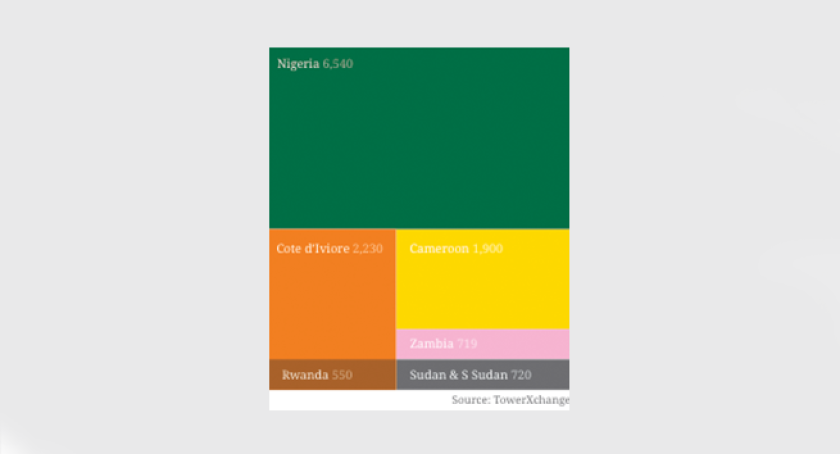

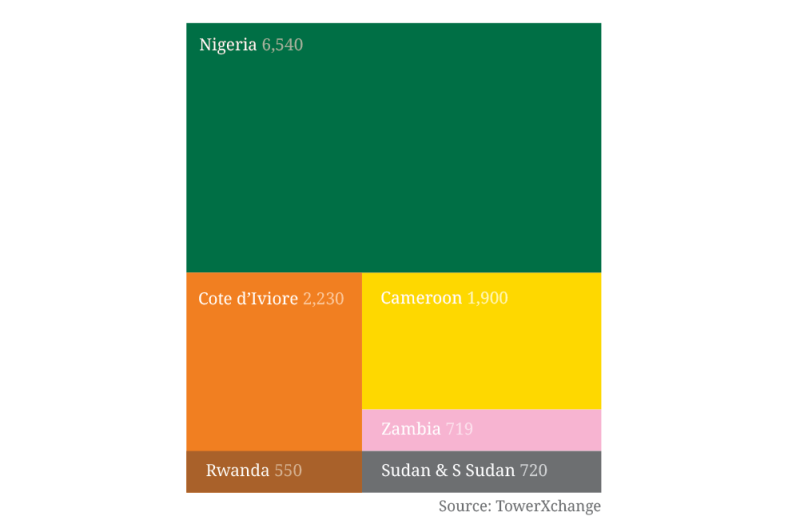

IHS has always made Nigeria a priority market, and they now own or manage 6,540 towers in the country, with a further 15,000 Nigerian towers for sale, for which Helios Towers Nigeria and, potentially, American Tower will compete fiercely with IHS.

The financial terms of the deal have not been announced, but Reuters cites banking sources suggesting Etisalat’s Nigerian portfolio was valued at around US$400mn.

The press release announcing the Etisalat Nigeria sale cites the usual drivers for network sharing; acceleration of 2G and 3G rollout, lowering costs, reducing diesel and increasing investment in alternative energy solutions. As well as releasing capital for Etisalat, IHS will improve network performance by leveraging its state-of-the-art Nigerian Network Operations Centre (NOC), which has enabled IHS to achieve uptimes of over 99% on its owned sites.

A US$100mn improvement capex budget has been set aside for energy efficiency initiatives and to upgrade structures and power solutions to accommodate additional tenants.

TowerXchange’s commentary on the enlarged IHS

Let’s take a step back and look at IHS after this transaction through the lens of a prospective investor in a future IHS liquidity event.

The majority of IHS’s capital value is derived from the 7,000+ African towers they now own. There is similar value creation potential in the 2,650 towers managed with license to lease, most of which are Orange’s towers in Cameroon and Cote d’Ivoire, but depending on contractual terms governing the end of that 15+5 year contract, IHS does not own the assets. IHS’s portfolio also includes a tranche of 2,850 managed towers, most of which are in Nigeria.

IHS’s tower count, already over 12,000 across Africa, may soon break the 10,000 barrier in Nigeria alone. To an investor, IHS is the leading Nigerian towerco with some valuable add-ons in West and Central Africa, providing comfort in diversification of country risk, whilst concentrating the value in Africa’s largest telecom market. IHS has done deals with credit worthy anchor tenants, MTN, Orange and now Etisalat, acquiring high quality sites that require less improvement capex for colocation than other towers currently for sale in Africa.

IHS may be the world’s fastest growing towerco, although it’s origins were modest. During IHS’s first ten years from 2001 to 2011, the company grew from zero to 270 sites. IHS then took off on an aggressive acquisition path, adding over 12,000 sites in the subsequent three years to today, converting this formerly modest Nigerian BTS and managed services business into the largest towerco in Africa. IHS’s growth isn’t all achieved through acquisition; the company delivered organic growth above 30% in the first three quarters on 2013, driven by collocation on existing towers and BTS programmes in Nigeria. By Q3 2013, EBITDA was around US$15mn on revenues of US$55mn for a 26% margin. IHS recently delisted from the Nigerian stock exchange so more up to date statistics are hard to come by.

What next for IHS? We expect IHS to bid aggressively for the remaining Nigerian towers. IHS may have an interest in extending their relationship with Orange in Senegal, Mali, Guinea Bissau and Guinea Conakry, where the towers are offered on a manage with license to lease basis. Of Airtel’s towers, Madagascar, Kenya, Zambia and of course Nigeria may be of interest to IHS. IHS may have a tower count over 20,000 by the end of 2015.

IHS are already big enough for an IPO, but there are no definite timescales for the next substantial liquidity event, and IHS has proved itself adept at raising capital. IHS has raised US$1.6bn to date, most recently from AIIM, Goldman Sachs and IFC GIF, joining existing shareholders the IHS management team, ECP, FMO, Korea Investment Corporation, Investec, IFC and majority stakeholder Wendel, who have participated in more than one round of capital raising.

IHS has acquired a reputation as an aggressive bidder in tower auctions. While their counterparties have realised good valuations for their assets, tower investment commentators consider the premiums that IHS have paid justifiable, such that IHS are considered the world’s greatest success story of a BTS-centric regional towerco transforming itself into a continental market leader.