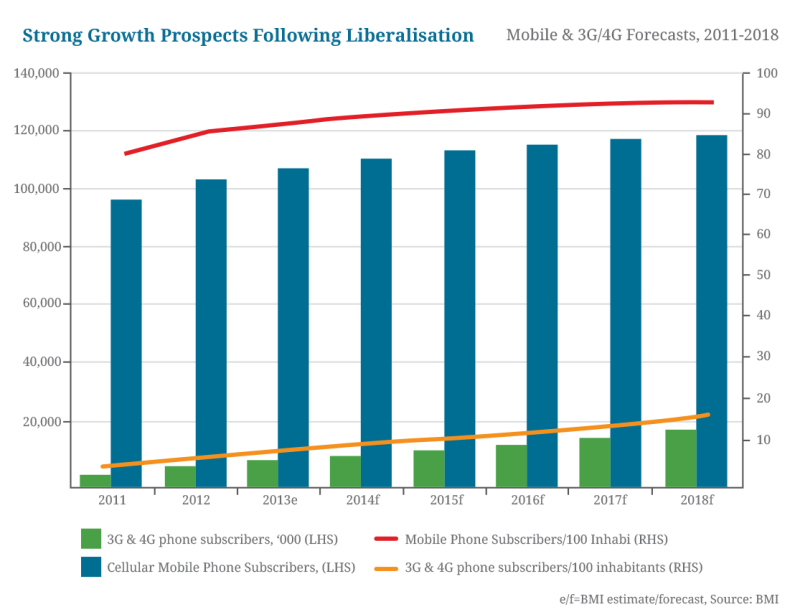

The next two years could prove to be a huge boon for the towers industry in Mexico, as regulatory, economic and business environment factors contrive to create a perfect storm for investment in the country. It is one of the more attractive markets from a telecoms perspective as it is the second most populous country in Latin America, with a population of over 111mn. However, it records one of the lowest mobile penetration rates in the region at 92.1%, according to BMI data as of September 2013. While most other Latin American markets are well over 100%, growth in Mexico has been held back by the dominant presence of América Móvil. Telecoms reforms signed into law in June 2013, combined with an increasingly strong private consumer, favourable demographics and a stronger peso due to an improvement in trade and investment dynamics, points to opportunities for growth in the Mexican towers industry.

Peña Nieto’s Reform Agenda To Encourage Competition

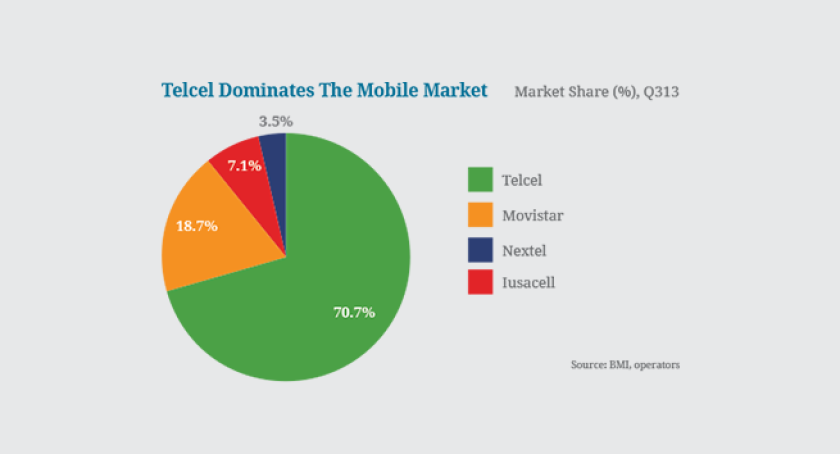

Growing social discontent seems to have forced the government under President Enrique Peña Nieto to address the multitude of monopolies and duopolies operating in the country and aims to reform the telecoms, energy and oil sectors. Monopolistic business practices in Mexico have long elevated consumer prices in sectors such as telecoms, television, energy and food manufacturing, weighing on middle class growth and exacerbating income inequality. For example, the OECD claimed telecoms giant América Móvil, which we believe serves around 80% of the country’s fixed-line market and 70.7% of its mobile phone market as of Q313, has regularly overcharged its clients by a total of nearly US$13.4bn annually.

BMI believes the dominance of América Móvil has led to a subdued tower sharing industry in Mexico, especially compared to the strong activity in Brazil and given Mexico’s close proximity to the US. Since end-2011 there have been nine major tower transactions in Brazil and only four in Mexico during the same period. Throughout Latin America, operators have generally reported falling ARPU levels and saturated penetration rates as they look for growth opportunities in rural regions. The costs of expanding infrastructure to these areas can be prohibitively expensive as a low return on investment and the cost of tower management makes it unattractive for telecoms companies. This has contributed to a rise in tower sharing through sale and lease arrangements that allow independent owners to run the communications infrastructure more efficiently, renting out access to all mobile operators at lower costs.

Mexico differs from the rest of the region because it is not characterised by market saturation due to penetration being at 92.1% and Telcel’s ARPU has remained fairly stable at about MXN167 since 2008. In Q313 its EBITDA margin was at 43.9%, far exceeding the 32.6% it posts for its total group operations and demonstrating the superior profitability of its Mexican unit. Of the four major tower transactions in Mexico since 2011, none involve the sale of towers by Telcel, with its smaller rivals Axtel, Telefónica and Iusacell instead being the selling party. Telcel’s dominant position allows it to be insulated from the industry and competitive trends, which are negatively affecting its rivals and therefore has no need to sell communication towers. Further, its dominant position is maintained by the national network it built through its fixed-line incumbent sister company Telmex, also owned by América Móvil. The lack of an effective policy has forced América Móvil to share infrastructure, selling towers to independent providers should allow Telefónica to access strategic sites outside of its coverage and this will therefore deteriorate América Móvil’s position. This limits the supply of communication infrastructure available for purchase by independent tower companies.

Mexican Tower Industry To Benefit

In a Q413 transaction between NII Holdings and American Tower, the mobile operator agreed to the sale of 1,483 towers in Mexico and 2,790 in Brazil. Despite there being a 1,300 difference in the number of towers, the price paid by American Tower was fairly similar at US$323.3mn in Mexico and US$413mn in Brazil. This works out to an average price per tower of roughly US$148,000 in Brazil and US$252,000 in Mexico. The price of individual towers can vary depending on factors such as foreign exchange rates, the strategic value of the tower location and coverage, as well as the type of technology utilised and the quality it provides. However, BMI data show towers in Mexico fetched a higher price than other major countries in Latin America, dating back to 2011. Selected data from major transactions in Colombia, Chile and Peru show prices for towers in the region vary from US$85,000 (Colombia 2011) up to US$280,000 (Mexico 2013). We believe this is again result of América Móvil’s monopoly, and the limited supply of available towers, but also the bureaucratic difficulties operators face when obtaining permits to deploy network infrastructure in Mexico and the lack of infrastructure sharing policy.

With telecoms reforms set to come into effect during 2014, the dynamics of the mobile market in Mexico could undergo a significant transformation and therefore present opportunities for the tower industry. The new regulatory authority, Ifetel, has been granted more power than its predecessor and will have the authority to order infrastructure sharing and even the break-up of Telmex and Telcel. Both scenarios present opportunities for tower companies as América Móvil’s superior national coverage will become less of an advantage. Rather than be able to set its own prices and charge excessively high mobile tariffs, it will be more exposed to competitive pressures and therefore more willing to sell infrastructure. Simplifying the process of obtaining permits for network deployment, combined with these reforms, should lead to more investment in the telecoms industry and see the average prices of towers in Mexico decrease.

In December 2013, Ifetel identified América Móvil as a dominant company in a preliminary filing, but will continue to investigate before pursuing tougher regulations. The decision was widely expected, but requires secondary legislation to liberalise the telecoms market, which has been delayed because Congress missed its deadline to implement them. News that the second round of legislation has been delayed does not bode well for the reform timeline as it will be pushed back until February 2014. The companies will then have until March to respond to the notifications and decide whether to challenge them. BMI still expects the secondary reforms to be passed, as the delay was due to a backlog of other legislation, rather than lobbying from special interests or a lack of political support from opposition parties. Mexico performs reasonably well in our short-term political risk ratings, owing to a relatively stable external profile and a benign inflationary outlook. Overall we do not expect a substantial deterioration in the country’s long-term political risk rating, which remains one of the strongest in the region due to a relatively stable constitutional framework and system of government.

Encouraging Macroeconomic Growth In 2014

We forecast Mexican real GDP growth to rise from 1.5% in 2013 to 3.5% in 2014, amid acceleration in household spending growth and an improvement in investment, bolstered by the successful reform drive in 2013. Exports will also pick up this year as US demand for manufacturing exports strengthens. We forecast a gradual appreciation of the peso to follow suit. Our expectation that monetary policy will normalise is predicated on a strengthening US economy, which will in turn bolster demand for Mexican exports and increase inbound investment.

The combination of regulatory developments and the forecast growth of the Mexican economy bodes well for the towers industry over 2014. Further, mobile operators are continuing their drive into next generation technologies. Nextel has pledged to invest US$3bn during 2014 to deploy LTE services, while Telefónica plans to increase its LTE subscriber base by 25%. We expect to see strong growth in 3G and 4G connections over 2014, helped by the undervalued Mexican peso, which looks set for a period of substantial appreciation and will bolster consumer purchasing power. Pending spectrum auctions for the 700MHz and 2.5GHz frequency bands will also contribute to advancing mobile broadband technologies and the need for continued investment and upgrade in network infrastructure should present more opportunities for tower companies in Mexico.

Possible downside risks that could impact this view, relate to the lengthy nature of these policy procedures, which have already been delayed to February 2014. Further setbacks will push the impact of the reform into 2015, with the possibility of appeals by the affected companies and spectrum auction organisation and rules needing to be addressed. If these scenarios can be resolved in a timely manner, the opening up of the telecoms market should see the cost of individual towers drop and allow América Móvil to participate in tower sharing during the next two years.